.svg)

.svg)

Biggest investment opportunity in history

Why Europe could miss its biggest investment opportunity in history

Europe is strong in talking: we want to become the first climate-neutral continent in the world. But when it comes to action, other parts of the world are faster.

1. A huge tech pool as a result of Europe’s research leadership

The EU’s R&D spend has created massive commercialization potential. The famous Horizon 2020 funds with R&D focus were allocated throughout the pilot period over the last seven years, with >40% going to climate-relevant R&D, totaling €25b. Many of these potential solutions will be crucial in saving our climate.

Europe is home to more than a third of the world-leading research institutes and universities. It also accounts for 45% of all patent applications worldwide.

2. The corporate demand is building up significantly

There is a tremendous demand building up for climate solutions, potentially amounting to history’s biggest investment opportunity. BCG Henderson Institute estimates the total global investment to reach net-zero to be $75tr.

High-tech accessibility, consumer demands, huge corporate pledges, and policy changes are unlocking steep market growth right now, as this PWC report finds. While American business leaders make more news, European industry giants such as Daimler, Siemens, or Schneider Electric have pledged to carbon-neutrality by 2040, IKEA and many others even by 2030.

Mind the gap: European investors are not yet prepared for climate tech.

Despite these converging factors and the opportunity to be bigger than ever, European investors are hesitant to reap the fruits of R&D investments. Only 5% of VC money invested in Europe goes to climate tech.

That’s not just any funding gap — only throwing more VC money at it won’t fill it. Instead, it will require some rethinking to capture the opportunity. Some characteristics of VC are incompatible with many emerging climate startups. This is for historical reasons. VC has become a highly optimized business driven by short-termism.

Here are the three main characteristics that prevent significant climate investments:

1. Venture capital has pressure for fast returns.

For VCs to be competitive in fundraising, they typically pitch their investors a fund multiple of >3x after 5–7 years. These numbers have not changed since B2C, software, and internet startups were the main focus of VC activities.

But climate startups need to transform sluggish, massive, and entrenched industries. Additionally, high technologies tend to have slower development and deployment cycles. Cutting-edge hardware engineering takes time, and so do challenges such as overcoming pilot purgatory with big corporates or operating in highly regulated industries.

2. Venture capital has the pressure for capital efficiency.

Well, time costs money. But adding to that, the very problems that make deployments of climate solutions lengthy also makes them costly — development projects, scalability engineering, challenging sales processes, and compliance.

That means that the milestones expected from a VC investment will cost more. Hence larger check sizes are required. Larger check sizes, in turn, require larger fund sizes than we have in Europe. Otherwise, you cannot sufficiently manage risk in an early-stage venture portfolio.

3. Venture capital lacks smart climate capital.

Smart capital is what startups call financial resources that come with non-financial benefits.

Deploying climate tech happens at the intersection of science, industry, and entrepreneurship. Each of these is crucial for successful design and deployments in each stage, from pilots to products.

VCs traditionally have strong roots in the entrepreneurial space. While they have been developing a more robust connection towards the industry over the last years (also with plenty of Corporate VCs joining the game), the scientific side, particularly in Europe, still needs to go a long way.

Conclusion: European VC funds aren’t made to invest in breakthrough climate ventures yet.

Today, European VC funds are not designed to play the long game that climate unicorns will need to win.

They don’t have sufficiently deep pockets to fund the capital needed for kickstarting a climate venture.

And they are not prepared for empowering their portfolio in the unique challenges that they face.

The European dilemma of letting the US and China drive disruption

Despite R&D in Europe promising one of the biggest opportunities worldwide, Europe is still only talking, while investors and founders from the US and China are already acting.

PWC found that the climate VC market has been growing steeply over the last years; in fact, even 3x more than the well-performing AI market. While this is generally good news, if we look at the key players, we see that much of the growth is driven by the big US and Chinese investors who invested roughly 4x and 3x more than Europe’s continent, respectively.

How much do we want to have the US reap the fruits of our R&D investments?

Over the last years, we have seen increasing participation of Silicon Valley VCs on European cap tables.

In the climate domain, US VCs offer better conditions for the unique challenges of climate startups. Looking at fund lifetimes, the US-based Gates-led VC Breakthrough Energy Ventures addressed this with a $1b fund of a 20 years lifecycle (and they are raising another $1.5b fund). This allows them to make deals no-one else can.

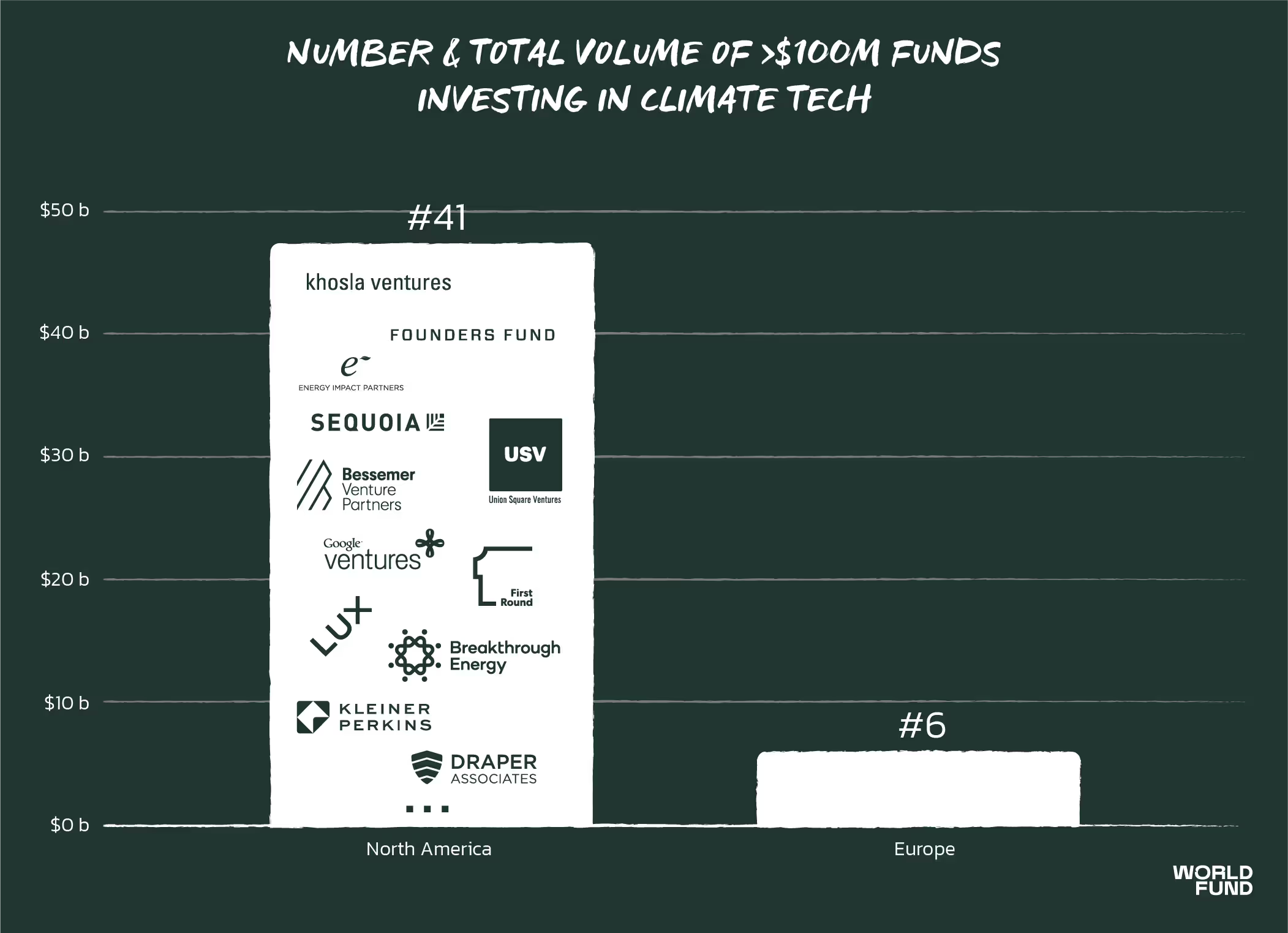

Regarding large checks: if we look at VC funds of >$100m that focus at least partly on climate tech, we significantly lack behind. Further, none of the 6 European funds in this graph is solely focused on climate, such as BEV or EIP.

If we zoom in on the US VC funds, we recognize that we can expect the image to become more drastic with Tier-1 VCs such as Sequoia, Founders Fund, Khosla Ventures, and USV joining climate tech because the VC market works in a winner-concentrating fashion. Startup success follows a power-law distribution. The median startup fails. The median VC performs well below average. The over-performing VCs get the entrepreneurs in competitive rounds to decide for them, therefore getting the best deals. As these VCs have it easier to raise more capital, the feedback loop begins, allowing them to make more and larger investments. Already today, European later stage startups don’t find capital in Europe, as one entrepreneur stated in this McKinsey paper: “We mainly spoke to US investors and SoftBank.”

If Europe is leading the climate agenda and the vision of the future we like — why do we let someone else handle the actions?

What Europe needs to succeed in climate tech: larger climate-focused VCs

There is a significant funding gap that needs to be filled with new types of VCs focusing on climate solutions.

We can see the first indicators that LPs understand the problem.

More money and attention are going towards pricing in climate as the most influential financial institutions are waking up companies because climate risk is a real business risk. Larry Fink even made it the focus of his annual letters to CEOs, customers, and BlackRock’s executives.

“We’re starting to see more evidence of climate change and its impact on capital allocation. I do believe that if you’re a long-term investor, you’d better frame all your investments through that lens.” — Larry Fink, CEO Blackrock

This will push pension funds, institutional money, funds of funds, and other investors to diversify. This means that more money could soon go to the VC asset class while also opening the market for climate-first VCs and transitioning towards data-driven impact reporting and forecasting on their portfolios.

It’s time to get beyond talking. Let’s act!

So there is hope that we in Europe will not let the opportunity pass us by: we should build the big climate companies of the future, finance them with European VC money, and let them become big in Europe. That would be not only good for us but also for the whole planet.

UPDATE 16.11.2020:

I stumbled upon another illustration showing that Europe has not yet seized its opportunity:

.avif)

.svg)