.svg)

.svg)

Seaweed deep dive article

.avif)

INTRODUCTION

Macroalgae, commonly known as seaweed, are multicellular, photosynthetic, marine organisms visible to the naked eye. Unlike their microscopic cousins, microalgae, macroalgae have complex structures resembling plants.

Over 10,000 macroalgae species have been classified, and are generally subdivided into three groups based on their pigmentation: red (e.g. dulse), green (e.g. sea lettuce) and brown algae (e.g. kelp and sargassum). These will vary in shape, size, and nutritional content, as well as affinity for coastal (30-50m) or deeper waters (up to 250m deep).

SEAWEED AS A CLIMATE SOLUTION

Macroalgae have been referred to as ‘nature’s superhero’, and the UN has called for a ‘seaweed revolution’ to help combat climate change. But how exactly is seaweed a climate solution? We categorise seaweed’s role in two key areas:

1. Emissions reduction via valorisation

» Displacing fossil-based products (e.g. bioplastics, bioenergy etc)

» Enabling methane reduction in livestock farming (e.g. as animal feed)

» Displacing animal or land intensive sources of protein for human consumption

There are also many positive co-benefits on the marine ecosystem

» Acts as an important habitat for a wide array of marine fauna

» Absorbs excess nitrogen and phosphorus from the water in which it grows, mitigating the marine threat of nutrient runoff from land based agriculture.

2. Carbon dioxide removal (CDR)

» Biochar production through pyrolysis (also a form of valorisation)

» Carbon export from seaweed cultivation, and sediment storage

» Sinking seaweed in the deep ocean to sequester carbon (either through wild collection or of harvested seaweed)

Seaweed is attractive as a climate solution due to several factors, including:

Low Resource Requirements: Seaweed doesn't require freshwater for growth as it thrives in abundant seawater; does not need fertilisers (which are mostly fossil-based); and it does not compete for land-use (e.g. with food crops).

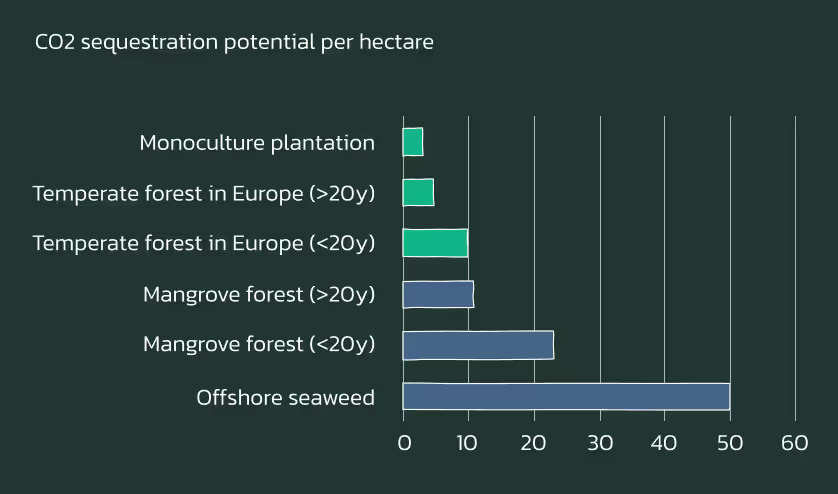

Fast Growth: Macroalgae have higher photosynthesis rates compared to terrestrial plants due to their efficient absorption of nutrients and CO2 from the water (e.g. giant kelp can grow 50cm a day, making it the fastest-growing plant on earth ).

Ecosystem co-benefits: Macroalgae can create a new habitat for diverse marine life, counteract acidification, and act as a water purifier by absorbing carbon, nitrogen, and phosphorus.

CURRENT STATE OF SEAWEED

Value chain

Whether macroalgae is cultivated for CDR or valorisation, parts of the value chain are quite similar, including:

1. Breeding and hatchery: to produce high quality and stable starter material, enabling the selection of specific seaweed strains, seedlings can be cultivated in labs and deployed once mature (e.g. Hortimare from the Netherlands or Pure Ocean Algae from Ireland).

2. Production: often based on a trade-off between cost, scalability, and accessibility:

• On-store farming in controlled environments such as water ponds or greenhouses (can ensure optimum growth conditions and processing, but high capex for the facilities and equipment as well as increased land use);

• Near-shore farming in shallow waters (5-50m) using substrate such as nets or lines. This is the most common type of seaweed farming (it does not use scarce land and has lower capex than on-shore, but with limited scalability and competing marine use cases for permit licences);

• Off-shore farming: similar deployment methods to near-shore, but requires boats or other mechanical devices to harvest (scalable, but more expensive to monitor and harvest, and exposed to wind, waves, and alien species);

• Co-location with wind farms or offshore facilities: benefits from labour and equipment synergies, making use of the “dead space” between offshore wind turbines (see recent projects announced by Denmark by Vattenfall and Norway by DNV/Equinor).

• Wild harvesting: collect the naturally occurring macroalgae in the ocean (can be the cheapest option, but supply is limited, often seasonal and potentially unreliable).

According to the Food and Agriculture Organization (FAO) data, the global seaweed output (both aquaculture and wild) has increased nearly three-fold between 2000 to 2019. Over 97% of seaweed cultivation (~31 million tonnes a year) is from marine aquaculture (mostly near-shore farming) of sea moss and sugar kelp from China, Indonesia and the Philippines. The remaining ~3% (1.1 million tonnes) is from wild harvesting, where Chile, Norway and Japan capture over half of the market.

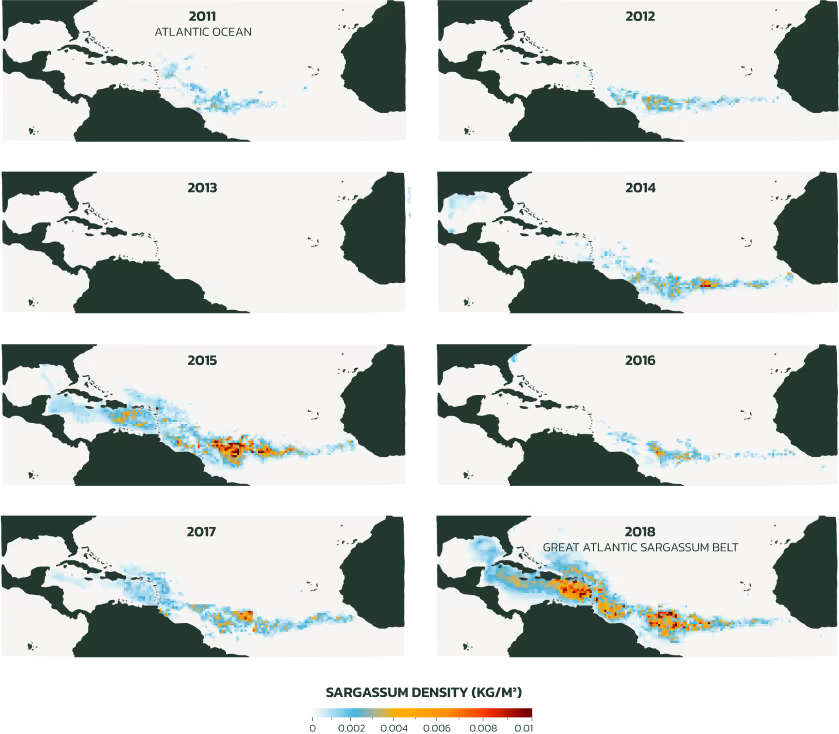

A major challenge with wild capture is the unpredictable nature of wild seaweed blooms. This is exemplified by Sargassum, the brown algae native to the Sargasso sea which has been washing up on the beaches of Mexico, Caribbean islands and Florida. The Great Atlantic Sargassum Belt (GASB) has been observed since 2011, extending 8,850 km from West Africa to the Gulf of Mexico, and weighing over >20 million tons at its peak. Its drivers are still being studied by scientists, but are likely due to a combination of factors, including nitrogen and phosphorus runoff from fertiliser, nutrient upwelling, and changing wind patterns and ocean circulations. Some companies, such as SOS Carbon, are trying to intercept the Sargassum before it reaches coastal habitats, where it rapidly decomposes and releases hydrogen sulphide and methane, affecting coastal marine ecosystems as well as tourism.

GROWTH IN THE GASB

POTENTIAL BENEFITS

Macroalgae cultivation for CDR through sinking can be an attractive prospect when considering some of the key parameters for any CDR company (see World Fund article on CDR), including:

Permanence: A key consideration for any CDR method is the durability of storage. Some companies (such as Seafields, Seaweed Generation and Running Tide) want to sink seaweed into the deep ocean to avoid the CO2 and methane release that would happen were the matter left to grow and die naturally. At depths greater than 1,000 metres, the biomass is subjected to high pressure and low temperatures, slowing decomposition and potentially locking away the carbon absorbed for centuries to millennia. This makes it a potentially more permanent solution than terrestrial afforestation, where sequestered carbon can be released back to the atmosphere quickly, for example due to wildfires.

Scale: As the ocean covers 70% of the surface area of the planet, it provides substantial potential to scale. The ocean is already incredibly effective at sequestering carbon through natural processes, as it holds about 50 times more carbon than the atmosphere and has sequestered about 30% of anthropogenic CO2 emissions . Studies vary in how scalable macroalgae cultivation for CDR is and the area required. The National Academies of Sciences estimates that for an annual sequestration potential of 100 megatons of CO2, an area of 73,000km2 (270 km per side) would be required - this would be roughly equivalent to the combined areas of Belgium and the Netherlands. Another more recent study estimated that we could grow enough seaweed to sequester 1 gigaton of CO2 annually within 1 million km2, which would be equivalent to only ~0.8% the world’s most productive exclusive economic zones (EEZs), where marine activity is under national sovereignty. For comparison, this would be less than the area occupied by all agricultural cropland in the US, which is ~1.6 million km2.

Cost: Another potential benefit is the cost of CDR. Even though sinking (terrestrial or marine) biomass in the deep oceans is relatively expensive today, it has the potential to be a relatively cheap nature-based solution at scale. Cost estimates from academic papers range from $480 to $1,257 per tonne of CO2 sequestered, and macroalgae carbon credits have been already been sold for $250/t (though mostly through pre-sales at a loss to catalyse the market). However, many startups expect they can get below $100/t by 2030 when deployed at scale. The US Department of Energy’s ARPA-E Mariner Programme even has a goal to reduce the costs to ~$75/t . Factors that need to be overcome to reduce these costs include (1) optimising farm designs to maximise lease space; (2) automating the seeding and harvest processes; (3) leveraging selective breeding to increase yields; (5) decarbonising equipment supply chains, energy usage, and ocean cultivation; (6) developing low-cost and accurate monitoring and reporting techniques.

Challenges

Despite the potential benefits of macroalgae sinking for CDR, there remain some challenges that need to be addressed before startups in this space become attractive investment opportunities.

MRV: First of all, it is about ensuring an appropriate monitoring, reporting and verification (MRV) system. Given the vastness of the oceans and the novelty in the CDR methods, it is essential to have standardised methodologies from third parties to verify uptake of atmospheric CO2 from macroalgae carbon sequestration. Currently, only Gold Standard has an approved carbon crediting methodology, purely for the collection of washed up seaweed to avoid the emissions from decomposition (and through valorisation), not for the cultivation of seaweed. However, Verra and Puro Earth are currently developing their respective frameworks for offshore seaweed farming and sinking, which will be key in building confidence in this space. In addition to the methodologies, there are also startups (e.g. Samudra Oceans) trying to automate and simplify MRV through digital and robotic monitoring systems. These are key to ensure that the seaweed is harvested in time, as seaweed can become a net carbon source rather than a sink in the late-growth and ageing stages.

Unintended consequences: The consequences of large scale primary productivity in the upper ocean for macroalgae sinking are still largely unknown . Potential areas of further study include for example potential nutrient competition with phytoplankton communities and other food web disruptions, possible methane release from deposition, risk of entanglement with marine life, and altering the chemical balance on the ocean floor when sinking is done at scale. Many of these risks can be mitigated, e.g. by growing seaweed in otherwise ‘dead zones’ to reduce risk of any nutritional competition. However, scientists still urge caution. In February 2024, a group of 19 leading scientists and researchers called for “an immediate moratorium on the sinking of seaweed biomass in the deep ocean” until its efficacy is established, and there is

robust, evidence-based assessment of its

sustainability.

Governance: Linked to the risk of unintended consequences, and the regulation of the high seas including the UN Convention on the Law of the Sea (1982), the London Convention (1972) and its modernised London Protocol (1996). Under the London Protocol, all dumping into the ocean is prohibited, except for acceptable wastes which may be organic material of natural origin. However, in October 2023, the London Protocol put out a statement on marine geoengineering, including seaweed cultivation for CDR, which requested for “activities other than legitimate scientific research” to

be deferred. As long-term scalability of macroalgae CDR would depend on offshore sinking, until a broad scientific consensus has been reached, and international governance has been established, there will be limited social licence to operate outside locally controlled watters.

EMISSIONS REDUCTION VIA VALORISATION

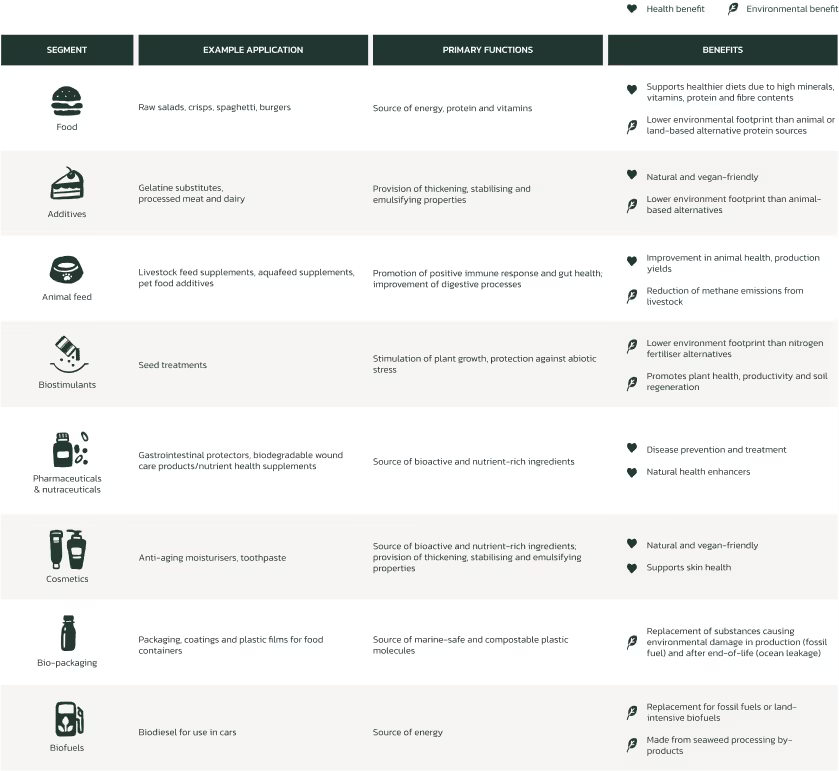

End-use market: Seaweed is very versatile and can be used across industries for a wide range of applications, including food, additives, animal feed, biostimulants, pharmaceuticals/ nutraceuticals, cosmetics, bio-plastics, and bioenergy. The current seaweed industry in Europe is focused on high-value, low-volume products with existing markets such as food and animal feed (e.g. GOA Ventures) being complemented now by a premium but nascent extraction market forming on the back of bioprocessing innovations (e.g. Oceanium and Origin by Ocean). However there is expected to be a growing demand for higher volume, lower-value products. In Europe alone, the biostimulant market could be worth up to €1.8 billion and bio-packaging up to €1.3 billion by 2030 , both industries that Carbonwave is addressing. It is through these high-volume products that seaweed production at scale could have a massive climate mitigation impact by disrupting incumbent fossil-based industries. For example, the emissions from the plastics industry today is around 1.8 Gt of CO2e annually , and from fertiliser it’s up to 2.6 Gt of CO2e.

DIFFERENT TYPES OF SEAWEED PRODUCTS

Cultivation: In order to scale macroalgae applications beyond the species and yield constraints of existing wild kelp ecosystems, macroalgae cultivation will play an important role in this market. In order to enable scale there are several key areas we must unlock:

• Cultivation Hardware: several technologies come together to enable consistent growth in the marine environment. The type of rope on a seeding line, the method and stage of adhesion of the seedling or spores, water quality data, the buoyancy and mooring systems, to the vessels used to seed, harvest and stabilise the crop. We are in an early but exciting stage of invention and innovation in the macroalgae market with large strides in productivity achievable as the tech stack matures. Companies such as Ocean Rainforest and Arctic Seaweed are pioneering this work in Europe.

• Genetics: improvements in seedling quality, growth profile and temperature resilience can together unlock yield and quality consistency towards specific en market applications.

• Permitting process: permitting can be a challenging and lengthy process. There is no standard process even within Europe. Regulatory transparency and standardisation will give visibility to cultivators, buyers and investors.

With quality and consistency of yield and clarity in the permitting process, comes the ability to unlock finance through the value chain which will ultimately unlock larger customers, market segments and scale.

Processing: Similar to its multiple end use-cases, seaweed can be processed in multiple ways depending on the end product. For example, it can go through drying before being consumed for food, thermochemical liquefaction to generate biofuels, and extraction as well as biofermentation for packaging materials. Even within specific processes themselves there can be multiple different pathways, e.g. extraction techniques for algae oil can be microwave-assisted, ultrasound-assisted, supercritical fluid extraction, or pressurised solvent extraction, among others. A key factor in determining the investment attractiveness of a startup will be whether they have any differentiating capabilities and technical know-how for the processing, or whether they are vertically integrated to reduce current supply chain risks.

WHAT DO WE LIKE

Business model

Revenue stacking by looking into different end-markets and use cases. In the short-to-medium term, due to the scientific uncertainties associated with seaweed sinking, the focus should be on valorisation. Over the longer-term, there can be more of a focus on CDR.

• Any startup looking into CDR, should have strong scientific partners, robust MRV systems, and a clear cost reduction pathway to sub $100/ton.

Value chain

Vertical integration (i.e. cultivating and harvesting) can de-risk the supply-demand imbalances, and capture a decent portion of the market in such a novel industry. In the absence of vertical integration, having offtake agreements from purchasers is key to validate demand.

Team operating expertise

Given the challenges in permitting and licences, having a track record of successful projects and securing local permits is essential to reach any meaningful scale.

Nature of seaweed projects

Cultivating different types of seaweed across different geographies can hedge against seasonal yield variations, as well as support business model diversification.

Deep dive available here.

.jpg)

.svg)