.svg)

.svg)

The Importance of Climate Tech for European Resilience

WHITE PAPER: THE IMPORTANCE OF CLIMATE TECH FOR EUROPEAN RESILIENCE

Full White Paper available here.

Europe stands at a critical juncture, facing unprecedented challenges that require bold action and strategic foresight. The series of shocks that have buffeted the European economy and strategic outlook in recent years - from the Covid-19 pandemic to the energy crisis and Trump administrations in the US - have tested Europe’s resilience, and exposed its dependencies and vulnerabilities.

Yet, these tests have also illuminated a path forward towards a resilient, decarbonised and more digitised economy - a path that requires sustained investment, innovation, and unwavering commitment to long-term goals.

This White Paper explores the multifaceted nature of European resilience and its profound implications for the investment landscape, offering insights and recommendations for policy action during this transformative period. The authors bring together the unique perspectives of three organisations: World Fund, a European climate tech venture capital firm; Kaya Partners, a political consultancy providing strategic advice on green transition policy; and Worthwhile Capital Partners, an advisory firm specialising in thematic investment strategies through funds and direct investment opportunities.

Executive Summary

For too long, Europe has depended on China for trade, Russia for energy, and the US for security. As the global geopolitical landscape undergoes profound shifts, Europe must reassert itself and establish resilience as a cornerstone of policy and strategy. The landmark 2024 Draghi Report highlighted the potential Europe has to adapt and thrive amid security, economic, and technological challenges. The interplay between the US, the EU, and China highlights an intensifying global competition for economic leadership, where industrial capacity, innovation, and strategic alliances are key determinants of influence. This competition underscores the urgent need for Europe to bolster its resilience through deliberate focus on both policy and investment.

The heart of this challenge lies at the intersection of national security and industrial capacity. A robust industrial base is not only critical for sustaining economic growth but also for ensuring autonomy in the face of geopolitical pressures. However, achieving this requires cohesive policy frameworks that can unlock investment at scale. Strategic policy, as a driver of confidence and derisking instrument, sets the stage for long-term investment flows, enabling the private sector to align with strategic national priorities.

We have pinpointed four critical sectors: energy, food systems and land use, frontier technologies, and raw materials. Each represents a vital pillar of European security and its green transition. This paper outlines key policy recommendations for each sector most likely to catalyse large-scale investment and actionable investment opportunities with high potential impact. At the same time, the overarching role of defence as a unifying thread cannot be overlooked, as ensuring security and stability amplifies the effectiveness of efforts across these domains.

“We have pinpointed four critical sectors: energy, food systems and land use, frontier technologies, and raw materials. Each represents a vital pillar of European security and its green transition.”

Energy: Decarbonising Europe’s energy sector is essential for reducing emissions, lowering costs, and ending reliance on imported energy while positioning the region as a leader in clean energy innovation and green industries. Key investment areas include grid modernisation to support decentralised renewable energy, scaling battery storage for reliability, advancing microgrids for local energy independence, and developing alternative energy carriers like hydrogen and synthetic fuels for hard-to-electrify sectors. An important measure the EU can take to enable this transition is the establishment of regional platforms for cross- border energy planning and investment, such as multinational grids and interconnectors, supported by collaborative funding mechanisms to ensure efficient energy distribution and sustainable growth.

Food, agriculture, and land use: Strengthening Europe’s food, agriculture, and land use sectors is critical for resilience, given their role in sustaining livelihoods, economic significance, and vulnerabilities to climate change and supply chain disruptions. Strategic investments should focus on reducing reliance on imported agricultural inputs, developing climate-resilient crops, adopting regenerative farming practices, scaling local protein production, and reducing dependence on imports. A vital policy measure that could be implemented to facilitate investment is reforming the Novel Foods Regulation to bolster the uptake of alternative proteins and foster innovation to reduce emissions and ensure long-term food security and sustainability.

FrontierTech: To achieve a decarbonised and digitised Europe, deploying frontier technologies like AI, biotech, fusion, robotics, e-aviation, space, and quantum computing is critical for reducing reliance on external sources and maintaining technological sovereignty and competitiveness. However, innovation is hindered by regulatory burdens, insufficient financing, and competition from foreign-subsidized products, threatening its leadership in emerging sectors. Mandating resilience criteria for strategic technology procurement and aligning trade and industrial policies can level the playing field, protect nascent industries, and attract investment to accelerate the development of strategic technologies like quantum computing, semiconductors, e-aviation, and space tech.

Raw materials: Critical minerals are essential for Europe’s green transition and defence industry, but pose risks due to heavy dependence on imports, particularly from China, which threatens supply chain stability. The Critical Raw Materials Act aims to reduce this dependence by promoting domestic production, recycling, and sustainable sourcing, but challenges remain in achieving the EU’s targets. We recommend implementing market de-risking mechanisms, such as contracts-for-difference, to stabilise the market and incentivise investment in raw material extraction and refinement. Investment opportunities focus on addressing critical raw material dependencies through diversifying supply chains, fostering innovation with regulatory support, and advancing circular economy solutions, including reducing resource usage, extending product life cycles, and developing efficient recycling technologies, with startups leading the way.

A GLOBAL RACE FOR ECONOMIC LEADERSHIP

In the late 2000s, Europe lost out on major opportunities that would have rendered the continent more resilient in the face of current geopolitical tension. Germany losing its early lead in the renewable energy sector is a key example of this. The proportion of electricity generated from renewable sources rose from 6.3% in 2000 to 25.4% in 2013 as a result of the introduction of the German Renewable Energy Law (Erneuerbare-Energien-Gesetz, EEG).1

The EEG was a huge success and more than 80 countries and regions adopted similar mechanisms, including Spain, Italy, France, the UK, the USA and China.2 It primarily relied on a feed-in tariff system to incentivize renewable energy development. Producers were guaranteed a fixed price for the electricity they fed into the grid, typically higher than the market price, for a period of 20 years. New companies like Q-Cells, SolarWorld, Conergy and REpower emerged in the fast-growing German wind and solar sectors employing 400,000 people at the peak in 2012.3 Germany was home to the world’s largest and leading producers of solar cells, modules, panels and wind turbines. The renewable energy producers began to capture a significant portion of the electricity market, reducing the market share of traditional utilities.4, 5

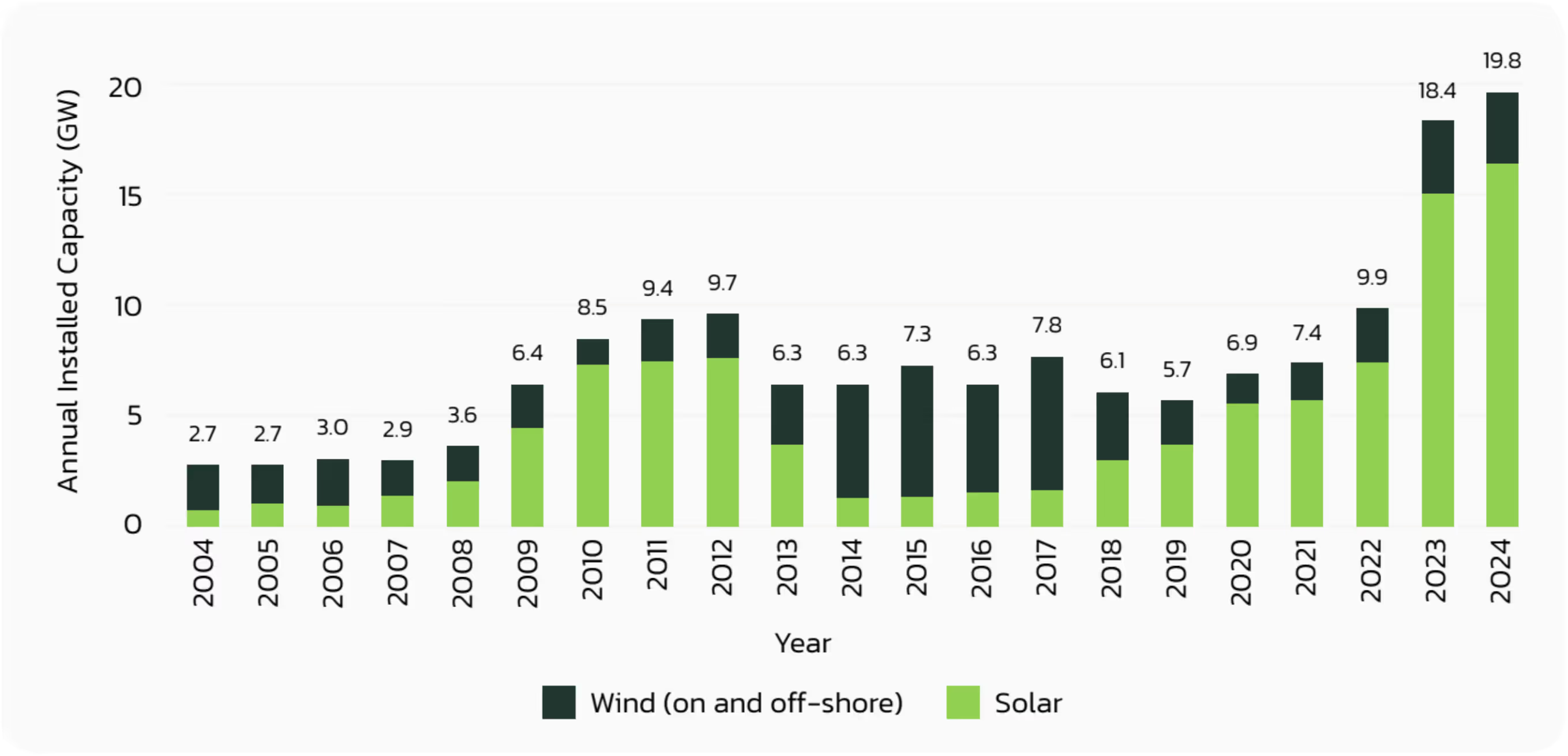

However, in the early 2010s incumbents like RWE, E.ON, and EnBW saw the profitability of their conventional coal, gas and nuclear power plants endangered by this progress (merit- order- effect)6. Following intense lobbying efforts from these incumbents, the German government sharply cut the feed-in tariffs and introduced caps on the subsidies. This led to a sudden decline in new capacity added. The annual installed renewable capacity, which peaked at 9.7 gigawatts in 2012, did not exceed that level until a decade later, reaching 9.9 gigawatts in 2022.7

Annual Installed Renewable Capacity – Germany

Germany’s world-leading solar companies filed for insolvency (i.e. Q-Cells and Centrotherm in 2012, Conergy in 2013 and SolarWorld in 2017), and most of the tech was sold to South Korean and Chinese companies, including the intellectual property rights.

A decade later, in an effort to wean itself off Russian gas, Europe’s energy sector once again invested heavily in solar power, with a 40% market growth in 2023.8 However, instead of being able to rely on domestic champions, Germany is replacing one reliance with another: photovoltaic imports from China. More than 86% of PV systems imported into Germany in 2023 came from the People’s Republic.9 Domestic solar production is almost non-existent. Even the imports from other countries contain Chinese components, as China dominates globally all value chain stages with market shares of up to 96%.10 By oversupplying the European market with subsidised consumer products and restricting the supply of materials critical to European manufacturing, China has been allowed to position itself to undermine European industry.

This example, where Germany recklessly relinquished leadership of an a rapidly growing industry,11 can unfortunately be seen in other sectors, too. As already indicated, a similar development is looming in the wind industry.

“Europe has a second chance to build up resilience, and climate tech must play a crucial role.”

Europe has a second chance to build up resilience, and climate tech must play a crucial role. The EU shouldn’t repeat the mistakes from the early 2010s, as today, even more is at stake due to the rising geopolitical tensions. This second chance even represents an unintended market opportunity: thanks to and based on its lead in climate tech R&D,19 Europe has more than twice as many climate tech startups and scaleups as the US: nearly 30.000 companies vs. 14.300.20

Cleantech International Patent Families (2017–2021)

However, innovative EU companies are still falling short of the financing needed to scale and commercialise their solutions.21 Venture capital financing in Europe has averaged only 0.2% of GDP between 2013-2023, a fraction of the US average of 0.7%.22, 23 Currently, limited European funding, for example, pushes e-aviation companies and battery manufacturers to seek support in China.24, 25 As geopolitical tensions rise, European manufacturers affiliated with China risk potential sanctions and obstaclesto their production dependent on Chinese-dominated supply chains.26 Robust European funding is therefore essential to secure a resilient, independent alternative.

You can access more insights, region-specific data, and all the takeaways by downloading the full Report below.

.png)

.svg)

.avif)