.svg)

.svg)

Green molecules, your next multi-billion dollar investment?

Green molecules, your next multi-billion dollar investment?

Green molecules may be tiny, but they represent a massive market opportunity. With the right investment, we could see multi-billion euro turnover companies emerge in this space within a handful of years.

Green molecules are energy carriers, synthetic fuels or other products produced with a low-to-zero CO₂ footprint. They include green hydrogen (produced via electrolysis using renewable electricity), green ammonia (made from green hydrogen and nitrogen), and synthetic hydrocarbons created by combining biological or atmospheric CO₂ with green hydrogen.

These new synthetic fuels will be crucial to the economies of the future, with some scenarios suggesting they could meet up to 30% of global energy demand by 2050. This is because there are sectors where electrification will fall short or prove locally uneconomic such as long-haul aviation, heavy industry, and deep-sea shipping. Even the IEA’s Net Zero scenario anticipates that more than 140 EJ of final energy consumption, over 40% of the total, will be met through non-electric forms in 2050. This includes liquid, gaseous, and solid fuels.

Beyond energy, common chemicals such as ethylene and propylene will also require green molecules as feedstock. Today, over 30 EJ, equivalent to around 5 billion barrels of oil, are consumed annually for these non-energy uses. This underscores the scale of demand: critical molecules already underpin an enormous global market, yet only a tiny fraction is produced sustainably.

If we invest in the right green molecule/e-fuel technology, we have the opportunity to make the next oil major entirely green. And this is not a pipe dream, we expect to see the formation of new, large-scale green molecule companies within the next few years.

Why molecules at all?

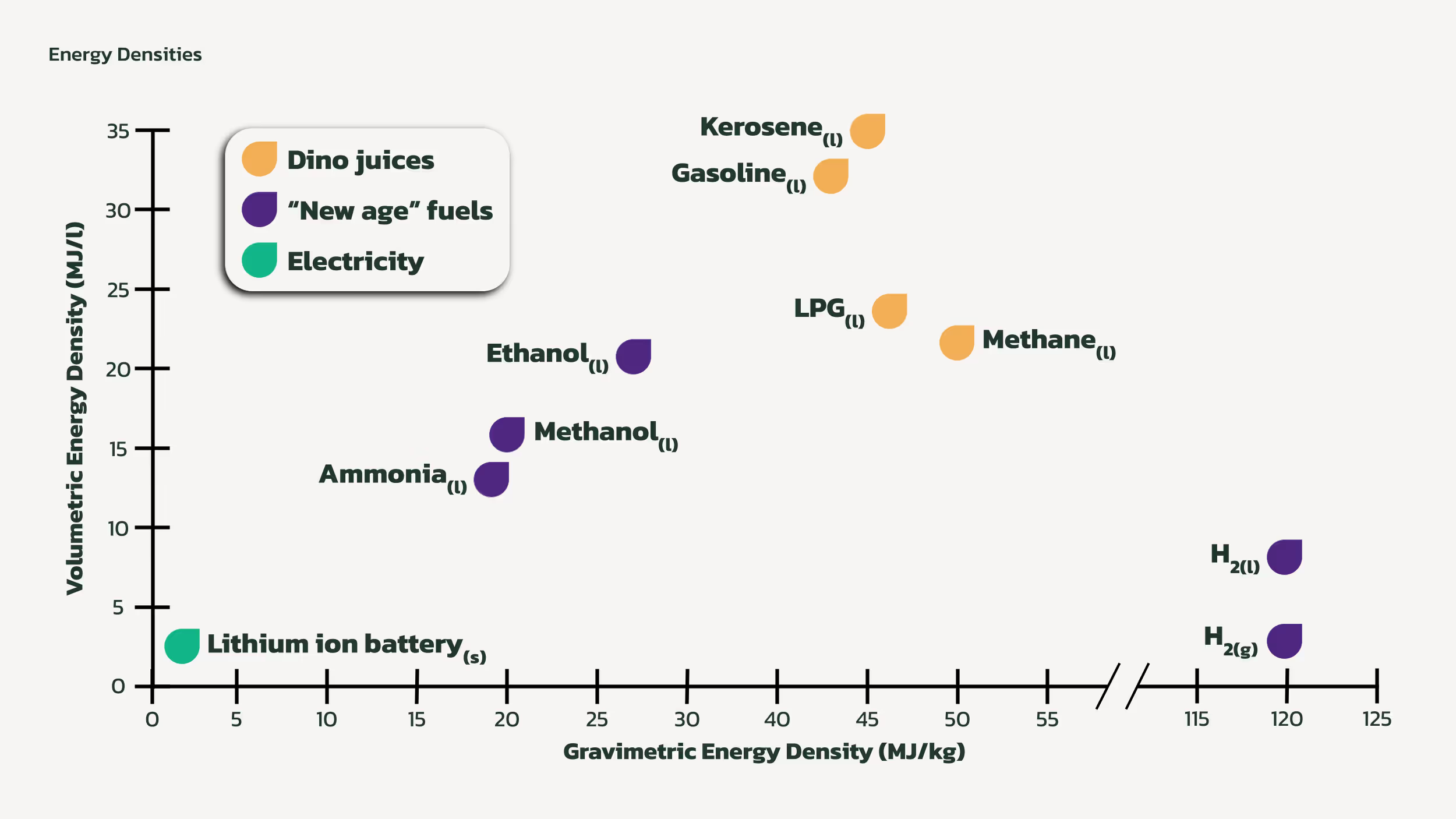

Molecules are valuable because they offer high (gravimetric and volumetric) energy density compared to batteries. Take the example of a cargo ship that must travel thousands of miles across the ocean. No existing battery technology could provide that range without severely compromising the ship’s carrying capacity and making the economics unworkable. By contrast, synthetic fuels can already substitute for heavy fuel oil on long voyages, although at present this remains an expensive option. The same holds true for aviation: with current and near-term battery technologies, only short-haul or regional flights are feasible, while long-distance international travel will continue to depend on liquid fuels.

Green energy carriers can also play a vital role in decarbonising sectors beyond transport. Industrial processes that rely on high-temperature heat, such as iron, steel, and cement production, are a prime example. In the future, they could even transform agriculture, with green ammonia replacing conventional ammonia which is responsible for over 1% of global GHG emissions.

These molecules are also exciting because they are easy and cheap to transport using existing infrastructure built for fossil fuels. Upgrading electrical infrastructure to be able to deliver equivalent power would be incredibly expensive, and these costs would have to be recouped somewhere. Just to put the contrast into perspective: if you were refuelling a shipping vessel with a standard fuel at 800t/hour, to provide the equivalent power electrically you would need 9 nuclear reactors, around 9GW of power, to refuel a single ship at a time.

A chance for Europe to mint a green Shell…

Europe is poised to lead the world into a green molecule-powered future. Green molecule production requires ample renewable energy resources and large quantities of space for solar installation without cannibalising farmland. Spain and Italy both fit the bill. The production process would create jobs and help revive rural economies in the regions even before delivering wider returns.

Europe is also the ideal place to start a green molecule company because our energy prices are so high. We are in such desperate need of new alternative energy sources, that we will likely be the first major market for green molecules (Japan, which also struggles with high energy costs, also presents a major market opportunity for any company in this space).

There is also a resilience factor at play. If Europe can scale up synthetic fuel production, we can increase our long-term resilience and protect ourselves from energy price fluctuation and supply constraints, a vital consideration against an increasingly unstable geopolitical backdrop.

And we are already seeing progress. Exclusive data compiled by Dealroom and shared with World Fund shows that green hydrogen startups have raised $6.8 billion globally since 2010. Data analysis reveals that Europe, the US, Australia, China and Canada are leading the way in developments, with 87 European green molecule companies raising $2.6 billion in the period.

Promising companies in the space include C1 Green Chemicals (e-methanol), Turn2X (e-methane), and Nium (green ammonia). While all are exciting from a decarbonisation perspective due to their green production pathways, perhaps even more compelling is their potential to achieve cost competitiveness with fossil-derived alternatives in the coming years. Although reaching cost parity still requires further technical development, the prospect of eliminating the current green premiums gives these startups the opportunity to truly redefine their respective industries.

The regulatory backdrop is also supportive of green molecule market growth. For example, the latest Maritime FuelEU regulations set emission reduction targets until 2050, and the recently announced ReFuel EU Aviation Regulation includes mandatory shares of sustainable aviation fuels (2% SAF in 2025, increasing to 70% by 2050, with a sub-mandate for synthetic SAF).

.avif)

The EU also recently announced a €100bn Clean Industrial Deal, which aims to support cleantech development with additional incentives. The deal includes an update to the InvestEU program that will see additional guarantees for funds focusing on industrial process modernisation, climate tech manufacturing and deployment, and energy infrastructure projects from 2025. All have a strong focus on affordability, which aligns well with green molecule market development.

… but challenges remain before we can reach this green molecule-powered future

Thinking this all sounds a bit too good to be true? You’re partially right. There are still several major challenges to overcome before the new green Shell or Chevron is minted in Europe.

The scale of renewable energy required to support green molecule production is enormous and is currently woefully insufficient. There are also significant infrastructure gaps that need to be filled before e-fuels can be adopted at scale. The CAPEX for synthetic fuel plants is high, and the “green premium” (the cost difference between green and fossil-derived molecules) remains too big, ranging from 100% to over 500% depending on the molecule.

.avif)

To create the next green molecule giant, we need to deliver more cost-effective green molecule production methods. We believe that this is both possible and a good investment opportunity.

There is a growing opportunity for synthetic green molecules because renewable energy production costs are continuing to decrease, and flexible green molecule production combined with process efficiency gains could reduce both the OPEX and CAPEX of large technical plants.

We believe there is also a real opportunity in biological routes to green molecule production, and direct solar-to-fuel technologies. Our analysis shows that both of these technologies, which are still in their infancy, could become competitive with biofuels at scale.

In short, green molecules represent an extraordinary emerging opportunity. The first company to bring an e-fuel to market at a cost comparable to fossil fuels, or even to biofuels, will be positioned to scale at an unprecedented pace. This not only presents a massive financial opportunity but also a powerful pathway to delivering a regenerative, sustainable future.

---

Are you a company innovating in this area?

These are the questions we at World Fund ask ourselves when looking at any new green molecule investment opportunity: Does it lower the green premium significantly? More than competitors? Is the production process able to handle intermittent energy input? Is the resulting fuel a drop-in solution for its intended use? Is there an existing market willingness to pay a premium? Can the process co-locate with cheap inputs?

Do you address some or all of these areas? If so, please get in touch at craig@worldfund.vc.

About Craig Douglas, Partner, World Fund

Craig Douglas is a Partner at World Fund. He has been investing in climate tech companies over the past 12 years at World Fund and SET Ventures, one of Europe’s longest-running climate funds. Craig has pioneered ESG and Impact in the venture community after creating a leading ESG framework in 2012, as well as co-designing a model which links impact to fund performance and compensation which is now used by over 50 funds. Craig is also an advisor to the EU Commission on Energy.

.svg)