.svg)

.svg)

How the energy sector will change

The power industry is our world’s engine, and it relies on fossil fuels.

This is part of a series where I want us to have a detailed look into how each high-emitting sector can change towards a regenerative world. From an investment perspective, I will do it by looking at major problems, the technologies that could solve them, interplaying trends, and the investment opportunity size.

The sectors we focus on in the series are 1. food, agriculture & land use, 2. energy (this article), 3. manufacturing, 4. construction, and 5. transportation.

In this article, if not explicitly linked differently, all facts and figures come from Project Drawdown, the latest IPCC reports, and tracxn data. The terminology “regeneration potential” refers to a solution area’s compatibility with our vision for a regenerative world.

We have a problem: The most carbon-intensive sector is the one that powers our industries and societies, and it will continue to increase.

It’s no understatement to say that the creation, distribution, and exploitation of energy as a resource has brought us to where we are today. Human progress is mostly built on using energy to solve complex problems or make things more convenient. But at the same time, our thirst for energy has put us into the most threatening global emergency in history.

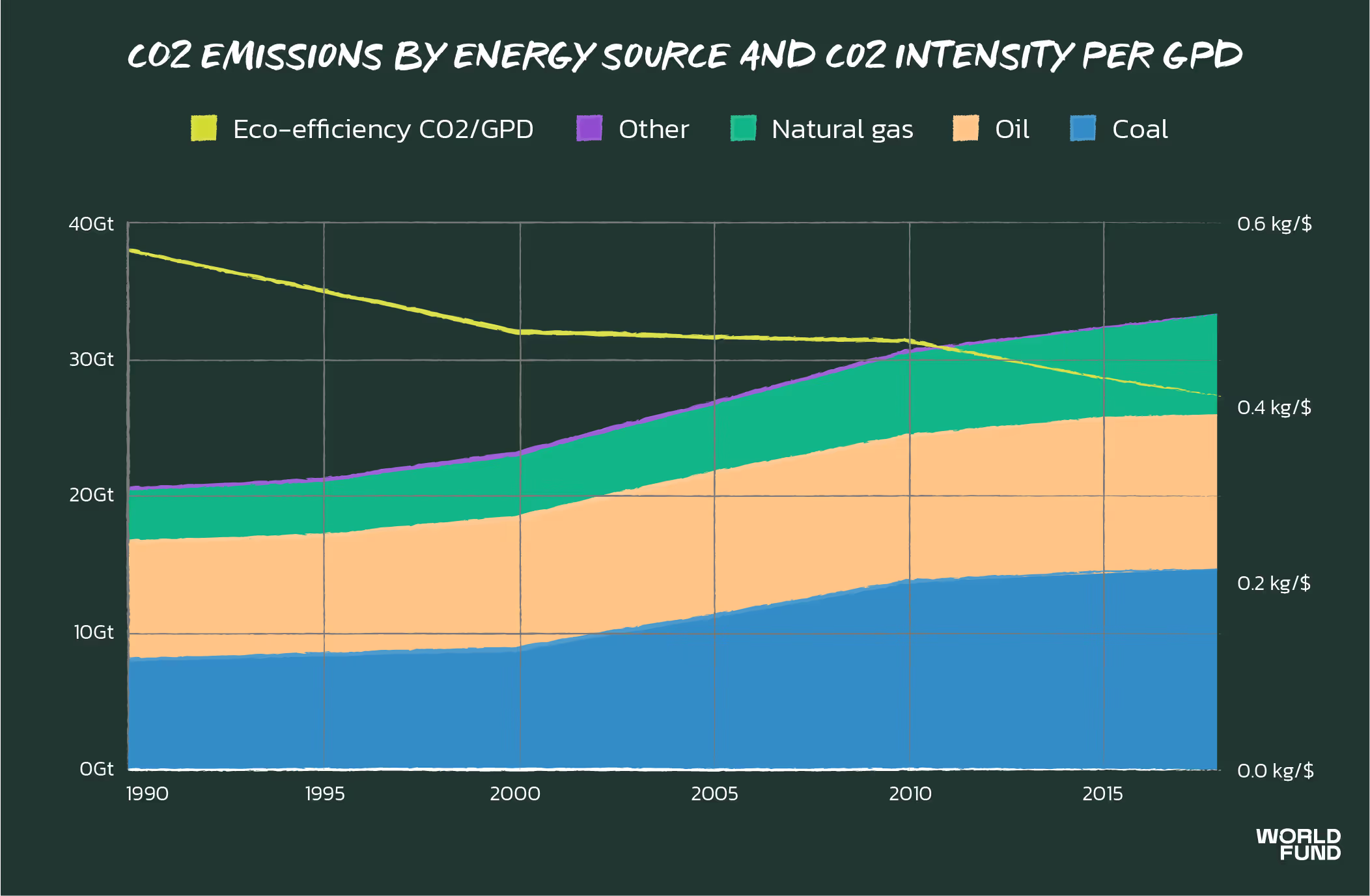

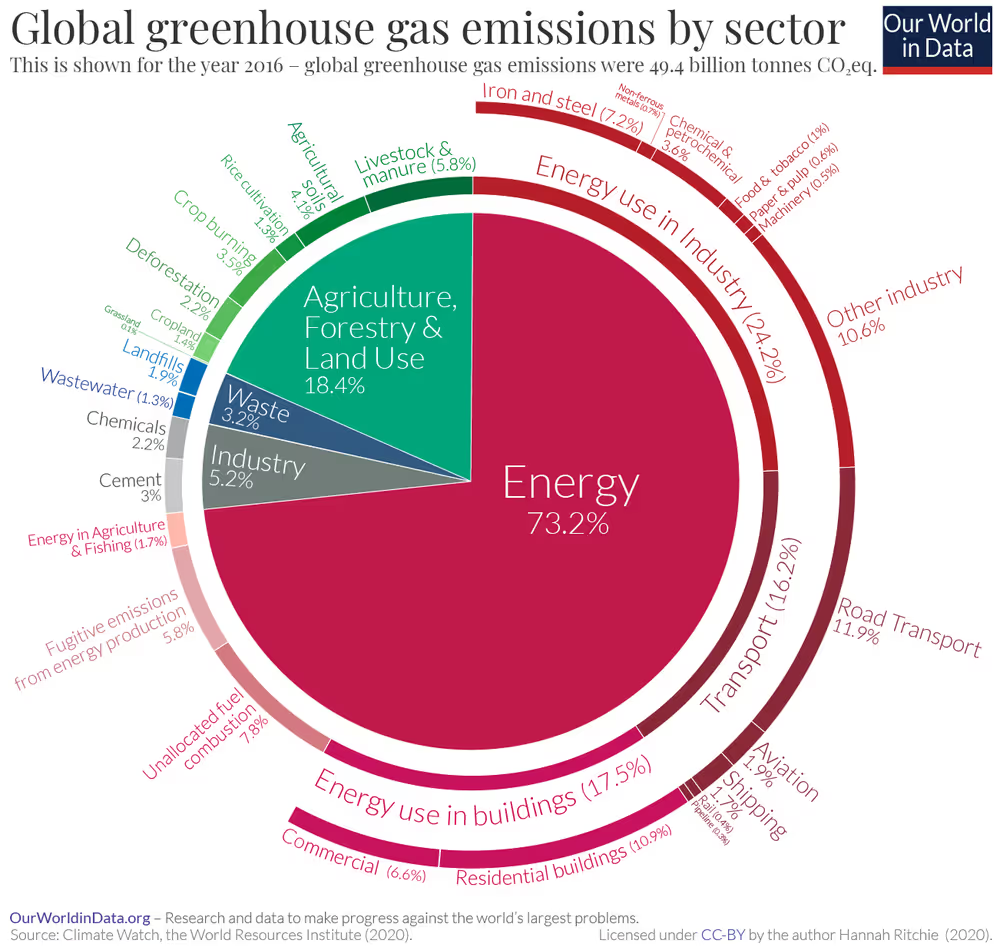

The reason is the way we produce our energy resources: Burning coal, oil, and gas to generate energy is inefficient and releases carbon — the IPCC associates 35% of global CO2e emissions with energy generation.

And we will not stop needing energy. Our global electricity demand is projected to double by 2050.

Transforming the power system is the necessary basis for all other sectors to reach their decarbonization potential.

An unprecedented transformation of a gigantic industry that is deeply interwoven with every other industry needs to happen.

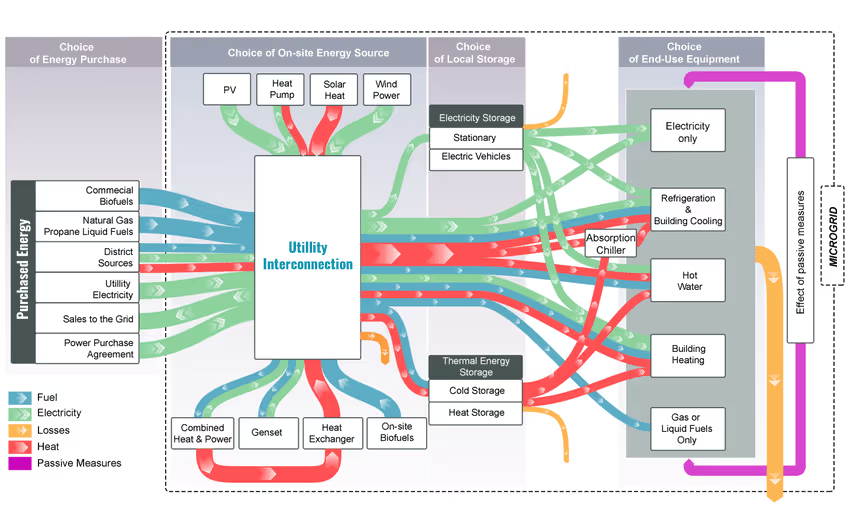

Energy has to be completely overhauled. While other sectors — such as food, ag, and land use — will be served a more substitutional and incremental approach, energy is already well into a transition towards a resource that will take a different role from what it is today. Energy will be

- renewable and abundant at marginal cost,

- generated decentralized with blurring lines between consumer and producer, and

- inherently volatile and dynamic in availability and usage.

Most current power infrastructure and economic and societal operations were not created and are not ready for that. But with every transformation, the dynamics of it unfolding will generate exciting tech solution opportunities, particularly startups. Each of the following solution areas comes with such opportunities:

- Renewable energy generation

- Transmission & distribution management

- Energy storage

- Efficient, flexible, and smart energy consumption

Solution area 1: renewable energy generation

Description

Generating energy with renewable sources such as solar, wind, hydro, or geothermal lies at the heart of the transformation that just started. Renewable energy systems will provide the cheapest possible electricity system by 2030, outperforming conventional power systems with a high margin (not even pricing in CO2e or similar).

Today’s renewables’ traction makes them, despite their low efficiency, already price competitive with fuel-based energy generation. The most recent IEA World Energy Outlook confirms solar to be the cheapest electricity source in history.

Regeneration-, market-, and GHG reduction-potential

In a regenerative world, we don’t have other alternatives to build our energy generation on. That is reflected in market demand, as well as the emissions reduction potential of renewables.

The GHG reduction potential is 123–322 Gt CO2e by 2050, according to Drawdown. Note that this calculation is interwoven with the other solution areas since they will mutually enable each other. And they’re all about enabling a renewable energy future.

However, established players will capture most of the renewable generation market. The two markets we expect to have the highest innovation potential are new materials for solar PV that will become a $56b-market by 2030, and advanced project planning and maintenance of renewable plants projected to be a $33b-market by 2030 based on our own calculation.

Tech enablers

The generation of renewable energy has seen a large tech innovation wave and has been scaling for a few years.

Now that many plants are productively operated, an opportunity is opening up for lowering operational costs. The key tech enablers are IoT and automation in smart production assets and drone and robotics technology — all coupled with big data analytics. For instance, wind generation machinery is exposed to harsh conditions and is costly in operation. The recently founded German startup Annea.ai is taking on the predictive and preventive maintenance challenge. The unicorn Uptake has been working on the same problem for Asian and US operators, proving the market need.

Take another example: While solar panels are less complicated machinery, they come with the challenge of less productivity over time once the dirt settles on them, particularly in high sun-exposure desert areas. Israel-based Ecoppia recently IPOed with their PV cleaning robots.

Another opportunity is lowering set up costs of plants, enabled through screening and designing tools for such projects with in-depth local data, low-cost, high-efficiency PV, and low-cost, high-efficiency microgrid wind systems. Notably, another promising tech enabler is within the base rate renewable: geothermal. Recent progress in drilling and heat transforming could lead to a more scalable approach for enhancing and repurposing existing oil and gas drillings.

We will discuss more enabling factors such as grid intelligence and cost-effective, scalable storage in the other solution areas.

Note: I don’t see fusion as a decarbonization enabling tech. I’ve fostered my opinion through regular conversations with Gregor Hagedorn and other Scientists4Future, who will publish their position on this soon (I will add the link here once published). They see a fully renewable energy mix by 2035 as possible and necessary.

Change my mind, but our future will be fully renewable, and we should focus on making that happen!

Market demand & investment landscape

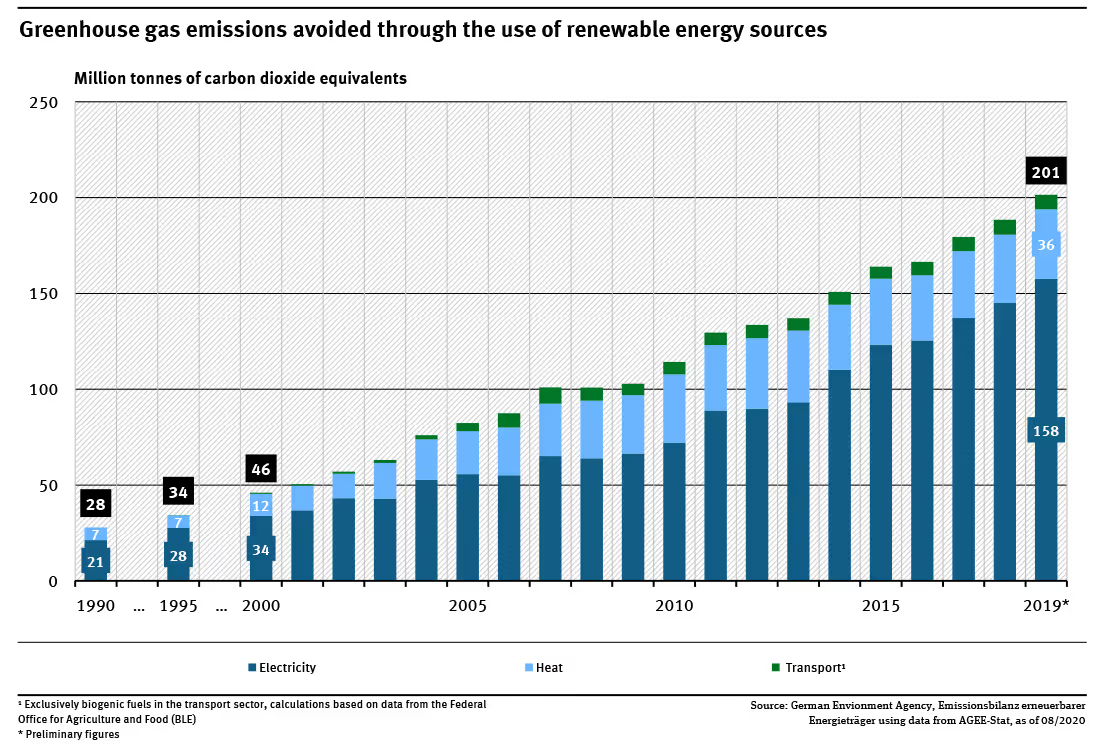

Good news: yearly, we avoid >200Mt of CO2e by existing renewables compared to a fossil fuel mix in Germany alone. Further, renewables will overtake coal to become the largest electricity generation source worldwide in 2025, supplying 30% of the demand.

Arguably, it’s not precisely for market demand but subsidies that have driven the significant share of generated renewable energy. But more rural and less electrified parts of this world now have a business case to adopt renewables due to the cost improvements driven by massive investments in pioneering countries.

Today, renewable energy is already the largest local energy production source in the EU. Still, it’s just the beginning of a much longer journey to bring renewables to power beyond electricity.

The key stakeholders are incumbents and governments. The venture capitalists are still only bystanders with occasional investments in accelerating technologies. Recent notable venture investments and exits include:

- Oxford Photovoltaics (UK, 2010), $82m Series A, led by Meyer Burger

- Amarenco (IR, 2019), $178m Series C, led by Tikehau and IDIA Capital

- Synergetik (FR, 2007), was acquired by Amarenco in 2020

- Sunnova (USA, 2010), IPO, 2020, market cap: $1.54Bn

- Ecoppia (IS, 2013), IPO, 2020, market cap: $300m

Solution area 2: transmission & distribution management

Description

With massive electrification, decentralization, and the adoption of renewables growing, so will the need for intelligent distribution, offer and demand balancing, and power quality management. This will challenge existing grids that will need to be retrofitted, while new grid tech will need to be deployed.

Regeneration-, market-, and GHG reduction-potential

We want to be efficient in a regenerative world with our consumption of the 100% renewable energy we create. But this is a mathematical problem that even increases in complexity if we add the constraint of 24/7 availability (particularly for mission-critical applications).

Experts, governments, and businesses alike agree on the need for robust and intelligent grids. Based on our calculations, the market is expected to be $300b by 2030.

The GHG reduction potential by 2050 is 55–106 Gt CO2e.

Tech enablers

The digitization of the grid matured over the last years. Tech is affordable and easily deployable for use cases that emerge in this fast-growing market. These enabling techs include smart meters, remote sensing, other IoT, and drones for measuring and steering, coupled with AI, machine vision, and widespread data connectivity for intelligent analysis and management.

Let’s take Overstory as an example. They serve utilities and insurances that face increasingly high financial and operational risks through more extreme vegetation events such as wildfires. They bridge the data gap by leveraging spatial, spectral, and temporal satellite data to provide real-time and predictive risk and maintenance insights.

Another example is Sympower that works on demand-side management. They connect assets, and their software allows grid operators to have more flexibility to manage these assets’ consumption.

As a last note: this solution area even has a significant space for incumbents that does not show too much innovation potential: retrofit 300,000 km of transmission lines and 10mn km of distribution lines for renewables and repurpose Europe’s 1000 GW of production plant assets (as well as retrofitting gas grids for CO2 and H2).

Market demand & investment landscape

Generally speaking, it’s grid providers that care about this solution area. In Europe, around €5b is invested in 1,000 R&D and demonstration projects and yearly €50b to adapt around this solution area.

On the venture side, grid complexity management has been an active VC investment field, particularly early-stage investments and low-capex deals with no or off-the-shelf hardware attracted investors. The most active investors are EIP with 8, GE with 4, Equinor with 4, and Almi with 3 deals. Recent deals in Europe and Israel include:

- Overstory (NL, 2019), $1.7 Seed, led by Pale Blue Dot

- AMMP (NL, 2017), $1.36m Seed, led by Point Nine Capital

- Heimdall (NO, 2015), $3.5m Series A, led by Lyse

- Sympower (EE, 2015), $3.3m Series A, led by Social Impact Ventures

- Senfal (NL, 2015), acquired by Vattenfall, undisclosed

Solution area 3: short & long term energy storage for small & grid scale applications

Description

A highly intelligent grid can only do so much. That’s why we will need buffering — additional flexibility for the grid — in the form of storage. This allows efficiently solving the mismatch of energy production and consumption. There is a need for short- and long-term storage depending on the grid context. Similarly, we’ll need a wide range of capacities.

Regeneration-, market-, and GHG reduction-potential

Here’s the missing ingredient to the previous solution areas to achieve a 100% renewable energy mix. Additionally, and more notable for this solution area, comes the need for a material design and a circular value chain that allows usage of safe and abundant materials, re-usage, and recycling — a regenerative system.

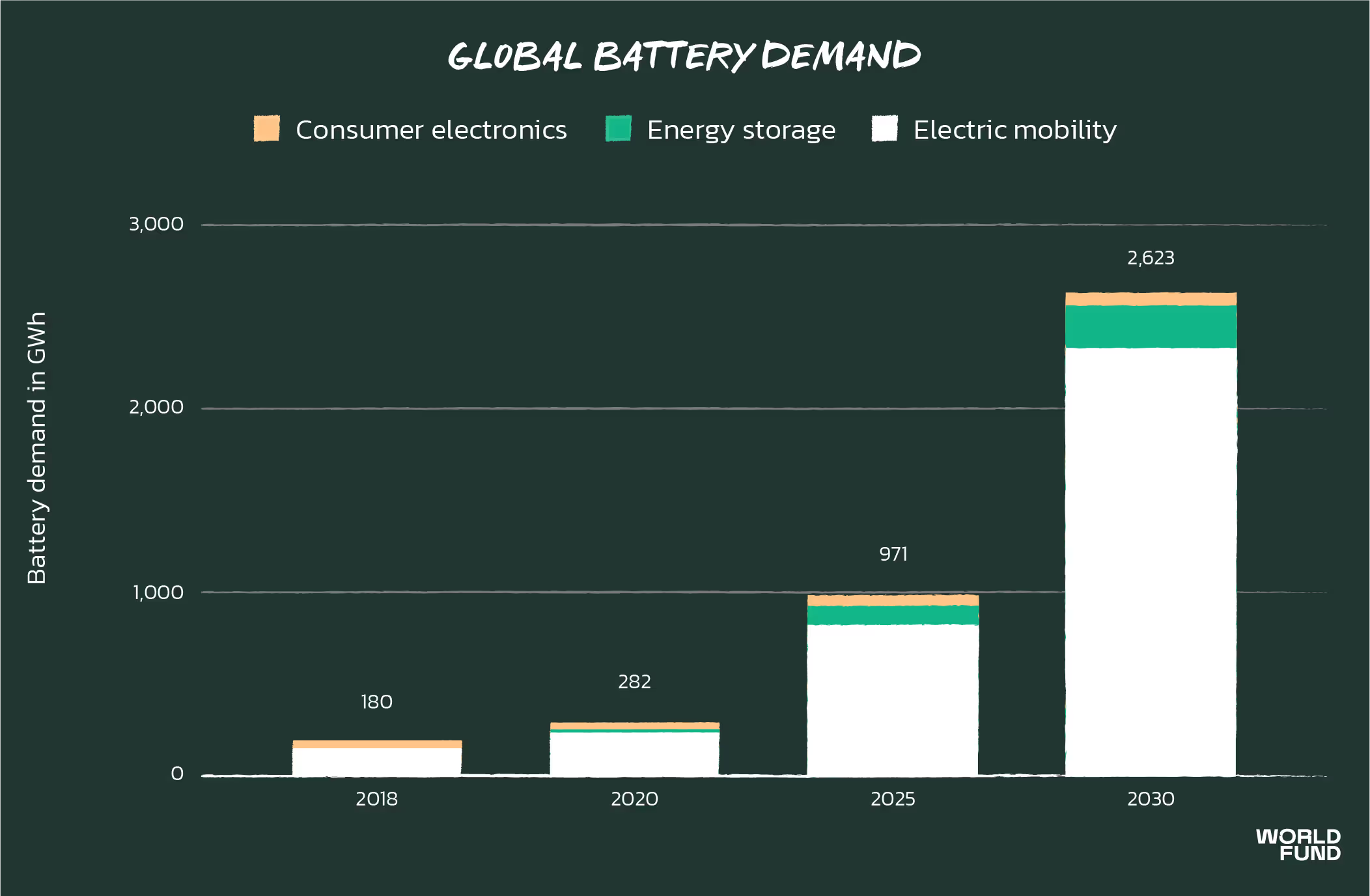

The critical role that storage will play in our renewable-powered and electrified future is reflected by the fact that we might need >150x storage compared to 2018 by 2050. The market size by 2030 is expected to exceed $400bn.

Note: The GHG potential (incl. its footprint) of storage is priced into the solution areas that it enables to work at peak efficiency. That is, generation, grid, and consumption.

Tech enablers

Storage requires different tech for different use cases. Today’s tech enablers are not close to sufficient for what we will need to scale our storage needs. Based on our calculations, in Europe, >80% of battery storage remains Li-ion. The most promising challenges remain to be solved in the lab: designing chemical and physical configurations to improve energy density, mastering new materials, and deploying a waste and contamination prevention strategy.

Many of these can be supported by new AI-based material study approaches (here’s a comprehensive Exponential View podcast episode). There’s also software and business model potential in managing storage-based services, but overall the opportunity to leverage for startups will be deep-tech.

The prime example in Europe is Northvolt, a manufacturer of batteries that wants to solve cost and scale. Founded in 2015, backed by the philanthropic capital of Norrsken, they have reached an estimated $1.64b of investments with Goldman Sachs and Volkswagen in the cap table. This demonstrates these startups’ capex heavy nature and how a new player can position itself in a gap overlooked by EU automotive companies.

As a younger example following a similar path, look at Addionics. They leverage AI-assisted design processes with 3D metal printing to produce fuel cell electrodes that 2–3x capacity and lifetime of batteries. If we look outside of Europe we find QuantumScape, also with Volkswagen as an investor, that recently had a SPAC and returned capital to its VC investor BEV — way before the fund’s end-of-life that spans 20 years.

UK-based YC-backed Holy Grail chose a platform approach to enable cutting edge ML for chemical and physical construction and optimization for energy storage designers.

Let’s see what disruptive energy storage technologies startups will develop that will make batteries more circular and enable grids to perform better.

Market demand & investment landscape

With trans-industrial electrification on its way, there has been a surge in deployed batteries. Mainly EVs have driven this growth. Also, the policy plans are steep — so is the growth within this decade.

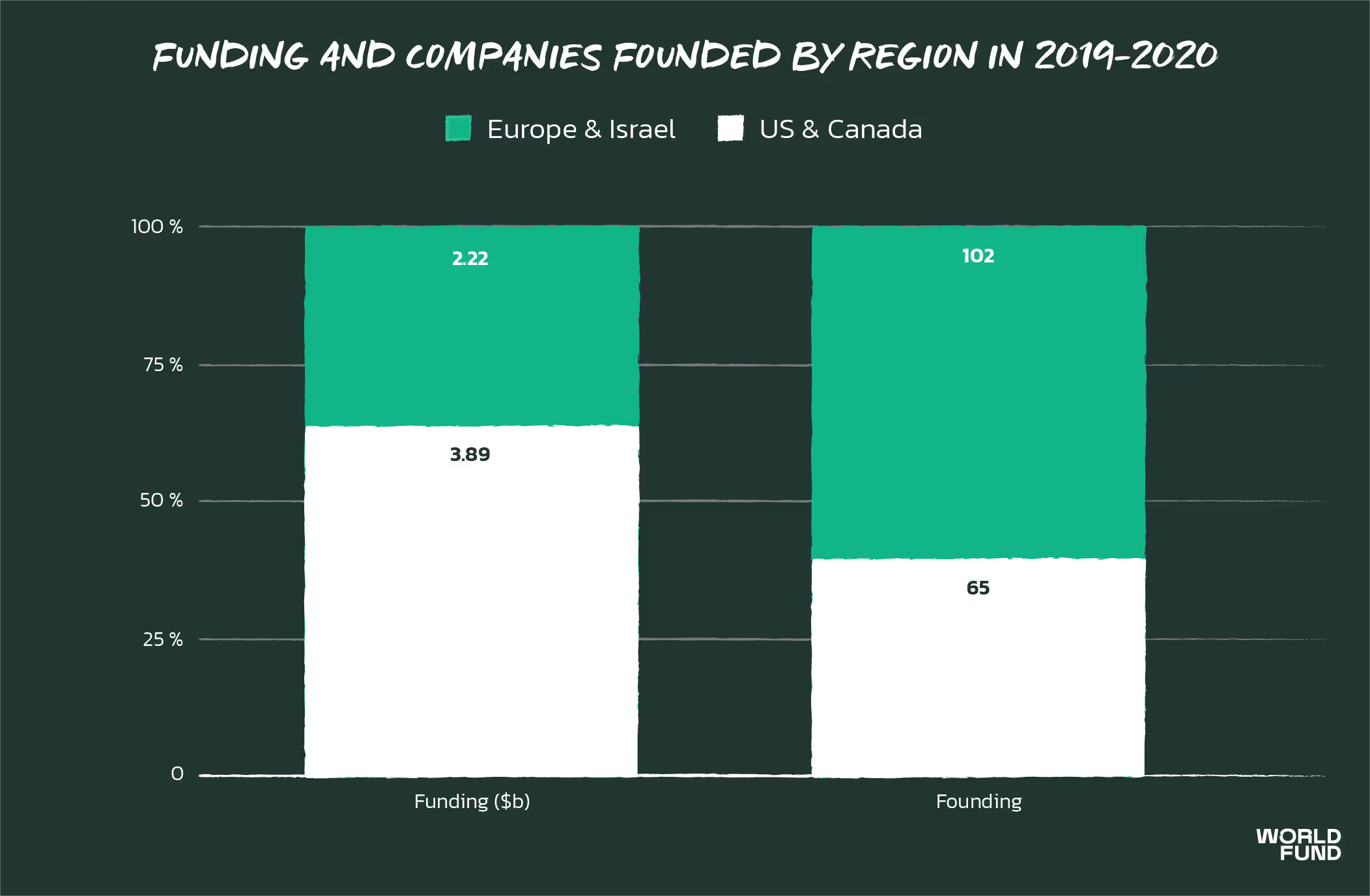

From 2018 to 2020, VCs invested $7.7b in this solution area. In Europe alone, 102 startups were founded in 2019/2020, 57% more than the 65 based in the US and Canada. 80% of the deals were early-stage, mostly seed-stage startups.

EU entrepreneurs lead creating the startups, but the US investors lead in funding (and owning) them with >50% of capital deployed to US startups.

Let’s hope that our engineering competence and startups will attract more (European) capital soon.

In 2019/2020, the most active investors of the solution area energy storage were Demeter with 4 deals and Hyundai with 6 deals. The accelerators InnoEnergy, Techstars, and YC took 13 startups. However, EU corporates are in the lead regarding acquisition activity: Engie acquired 4, Total 3, Shell 3, and Statkraft 3 companies. Some notable recent deals include:

- Northvolt (SE, 2016), $600m Series C, led by Goldman Sachs & Volkswagen

- Highview Power (UK, 2005), $46m Series C, led by Sumitomo

- Skeleton Tech (EE, 2009), $48.5m Series D, led by InnoEnergy

- Energy Vault (CH, 2017), $110m Series B, led by Softbank

- QuantumScape (US, 2010), SPAC, 2020, $3.3bn valuation

- Maxwell Technologies (US, 1965), acq. by Tesla, 2019, $218m

- Sonnen (DE, 2010), acq. by Shell, 2019, undisclosed valuation

Solution area 4: efficient, flexible, and smart energy consumption

Description

Lastly, we look at the consumption nodes in the grids. This is where it gets exciting: their role is to become efficient consumers and leverage new ways of operating and supporting their grid in managing its complexity.

A particularly interesting set of consumption nodes are so-called distributed energy resources (DERs) to balance intermittent renewable loads similar to decentralized storage and production. Connecting millions of devices communicating in real-time gives rise to exciting mathematical problems for dynamically managing this system. This gives rise to entirely new business models, unlocking a renewed energy system’s real power.

Regeneration-, market-, and GHG reduction-potential

This solution area is a corollary of connecting renewables to the grid and, therefore, part of our regenerative world. The market will consist of many previously unseen business models and based on our analysis will grow to >$100b by 2030.

The GHG potential is significant. Without double-counting renewables generation, microgrids, or EVs, which are counted in the respective solution areas, it sums up to 63–93 Gt of CO2e by 2050.

Tech enablers

The tech enablers are affordable and partly deployed, such as smart meters, real-time consumption data, and IoT assets. Big data and network technologies will allow intelligent management. A prime example of this was Google’s AI-driven energy optimization of their server farms with AI resulting in a whopping 40% reduction. Next, startups will make this accessible for non-AI incumbents.

One startup that wants to empower households to benefit from intelligent energy management is Tibber. It connects devices and allows households to favor renewable energy sources and overall reduce their energy cost. GridX goes even a step further, looking to become a platform for grid services.

Startups like Bboxx aim to supply 15% of the world’s population with no electricity access with reliable, decentralized, and clean electricity. A much younger startup, mPower, seeks to solve the same challenge with a B2B2C model enabling locals to sell off the shelf solar and storage. Due to Covid-19, the number of people without electricity access is expected to grow according to IEA’s Energy Outlook 2020.

The business models enabled through these technologies, particularly the increase of DERs, are smart tariffs, distributed energy trading, aggregation platforms, and energy services. An exciting new market will enable residential communities or micro SMEs to monetize their energy generation and DERs.

Market demand & investment landscape

Energy suppliers are at the forefront of driving this solution area. They have a strategic need to prosper in the energy transition by acquiring new capabilities and survive the complexity of interconnected DERs. On average, European energy suppliers spent >€120m p.a. (~6% of their total investments) acquiring startups from 2016–2019.

For this reason, IPOs tend to be rarer, with startups favoring strategic exits. The recent trend around SPACs (special purpose acquisition companies) might change this trend by allowing startups to go public earlier. Energy SPACs are already ticking up.

Investments revolve around virtual power plants, efficiency, and grid resources management. The most active investors are E.ON with 5, Samsung with 3, EIP, Equinor, and Techstars with 2 deals. Selected recent deals in Europe and Israel:

- Bboxx (UK, 2005), $50m Series D, led by Mitsubishi

- Tiko (CH, 2012), undisclosed Series A, led by Engie

- Eliq (SE, 2010), $5.9m Series A, led by Contrarian Ventures and Inven Capital

- Tibber (SE, 2016), $65m Series B, led by Balderton Capital and Eight Roads

- mPower (CH, 2017), $409k Seed, led by InnoEnergy

- Enpal (DE, 2017), $100m Series B + venture debt, led by Princeville Capital

- Limejump (UK, 2013), acquired by Shell, undisclosed

Let’s shift gears in the energy transition and double down on the opportunities of an all-renewable power generated world!

As we’ve seen, this sector’s transition is well underway, with investments for the first time surpassing $500b p.a. (incl. electrified transport). We see significant challenges and opportunities. And if we look at the investment and acquisition activities, one question arises: will the incumbents that have made their fortune on fossil fuels become the incumbents of our regenerative world?

Whatever the answer, founders, startups, and venture capital have to drive this transition. As the past has shown, only with the power behind venture capital can we achieve the speed needed for our economy’s transformation. The social and financial opportunities are gigantic. Let’s speed up!

.svg)