.svg)

.svg)

Robotics: Europe's Industrial Comeback?

Robotics is shifting from “Can we build it?” to “Can we deploy it?”

At World Fund, we have spent the last few months diving into the world of Robotics and Physical AI, speaking with dozens of founders, researchers and investors across the ecosystem in Europe and beyond. This piece aims to distil some of the key messages we have identified and highlight where we see the biggest opportunities.

For over a decade, the fundamental challenge in robotics was technological: “Can we build it?” Robotics was generally something confined to conventional manufacturing assembly lines, focused solely on task-specific automation.

Things have moved on rapidly.

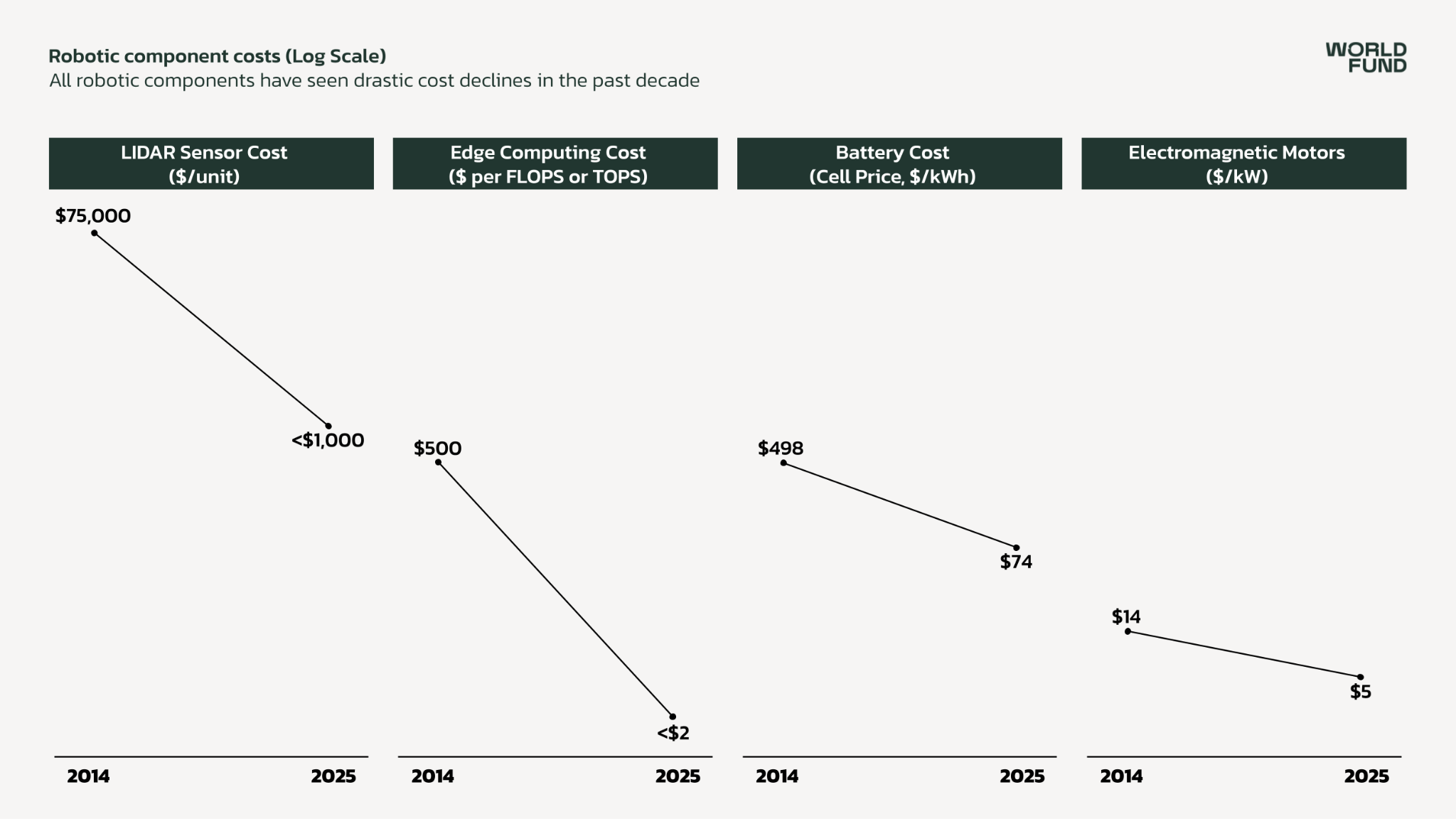

Learning curves for batteries and compute have continued driving down costs for essential robotics components. Sensors that used to cost $75,000 ten years ago now cost less than $1,000. At the same time, performance of these components has continued to improve, enabling significantly better capabilities, from motion sensing and depth perception, to load-bearing and force feedback.

Today, the building blocks of robotics are better than ever and cheaper than ever, which is enabling the rise of more generalisable robotics.

The question has now started to shift towards: "Can we deploy robots cheaply, reliably, and at scale?"

This is ultimately an economics question, not an engineering one. It means the ability of companies to deploy robots into the real world quickly will be imperative.

Economics: The real cost isn’t the robot

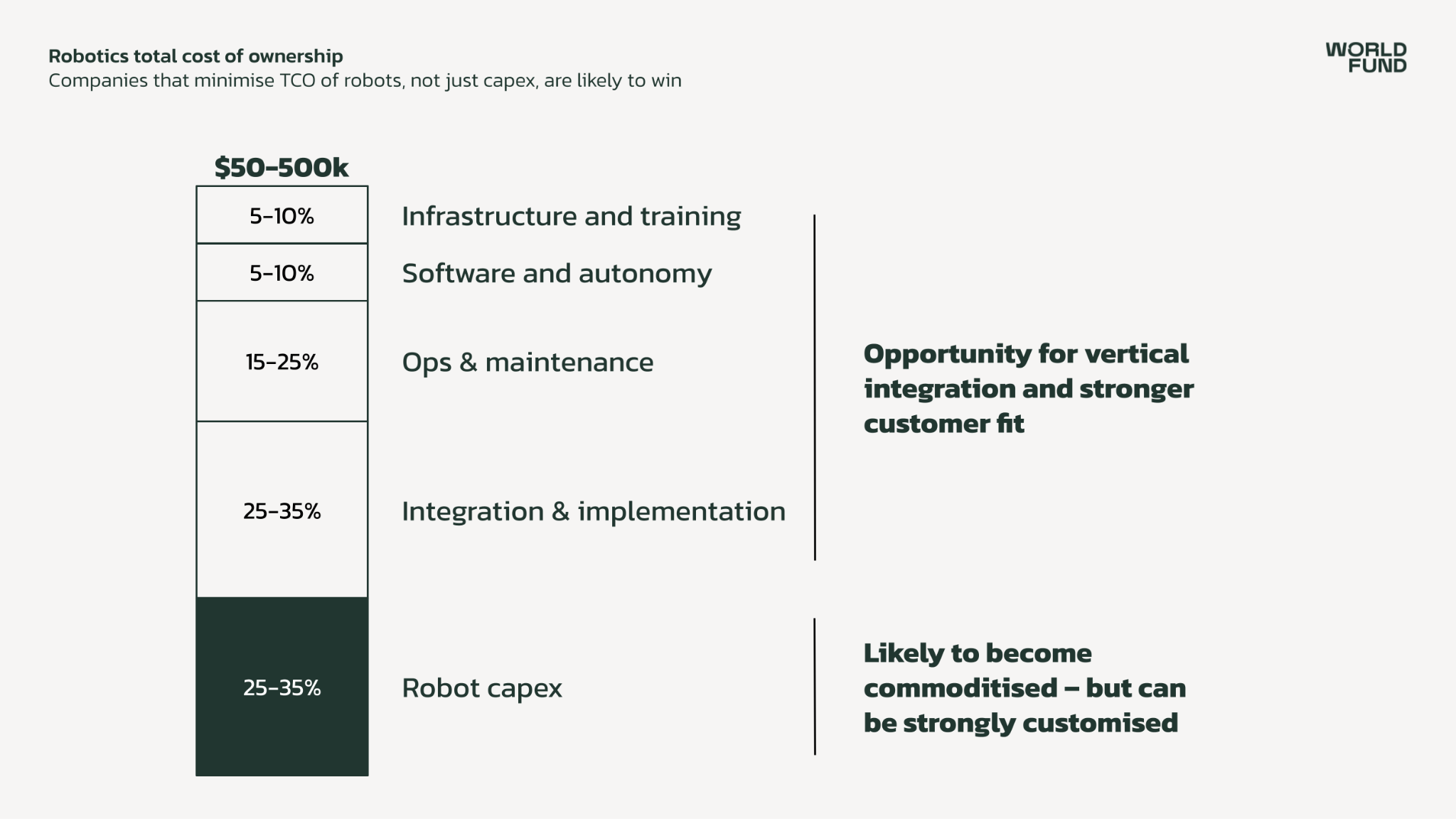

The most pervasive misconception in robotics (one that we were guilty of before diving into this topic, too) is that a lower upfront robot cost automatically means successful deployment. It does not.

Based on our research and conversations, we estimate that hardware for advanced robots accounts for around 25-35% of the total cost of ownership, though this can vary strongly depending on the end-application.

As the chart above shows, advanced robotic hardware is becoming increasingly commoditised – just try searching for a lidar sensor on Alibaba. There is one clear exception: actuators are still pricey, and often require a tricky amount of customisation for specific uses. However, we are bullish that costs will eventually come down here, too.

Ever-cheaper hardware has led to two emerging trends.

First, it has highlighted how the real challenge is “everything else”. Much as we have seen soft costs dominate overall levelised costs for solar (where hardware has become unbelievably cheap), a similar principle applies in the case of robotics.

Companies that relentlessly focus on reliable, seamless integration will be the ones able to deploy more robots, faster. This means a focus on ease of operations, redesigning workflows simply, reducing downtime, fast maintenance, and the wider problem-solving required to make a robot function reliably in the real world. A lack of focus on integration and solving urgent customer needs contributed to Rethink Robotics, a startup building industrial cobots, struggling to gain traction and ultimately folding in 2018.

Second, advanced robotics and automation are becoming commercially relevant in an increasing number of end-use markets – but are still determined strongly by return-on-investment calculations. A warehouse operator does not need a robot to replace 100% of human labour to justify the investment. In such an environment, it could be that replacing just a third or a fifth of human tasks (and working hours) is enough to make the ROI calculations pan out.

The proof of this trend is visible: Amazon's employee headcount has remained flat since 2022, even as its robot deployments have grown steadily. Customers across logistics, manufacturing, and warehousing demand payback periods of just a few years.

.png)

Deployment is also, for now, concentrated in sectors where four conditions align: high labour costs, acute labour shortages (in some cases as a result of rapidly growing demand), low productivity, and sometimes strong regulatory drivers. Together, these lead to compelling ROIs for robotic deployment. Logistics, warehousing and certain parts of manufacturing lead now, but a much wider range, from pharmaceuticals to semiconductors or construction, is likely to follow soon.

These sectors do not require general-purpose robots. They require solutions that are economical and reliable enough to replace human workers in specific, repetitive, or dangerous tasks: palletisation, material handling, multi-component assembly, and so on.

Europe’s value proposition: a world-class base to build an entire robotics ecosystem

The robotics supply chain is tiered. At the bottom are component manufacturers: actuators, motors, sensors, structural materials and so on. Subsystems and middleware providers sit in the middle. At the top are system integrators and end-use application companies.

Europe is already very strong at both the bottom and top layers of this ecosystem: think of German precision components, Swiss subsystems, and French electronics manufacturers. European customers in construction, manufacturing, and energy infrastructure also represent real demand pull for startups across Europe.

All of this is supported by a world-class research ecosystem: ETH Zurich, TU Munich, Imperial College London and others generate both breakthrough innovations and the talent pipeline that feeds the startup ecosystem. (This is a good point to give a shout-out to the newly-launched European Student Robotics Association!).

The constraint for Europe will be iteration speed.

China's robotics ecosystem has developed world-leading clusters concentrated around Shenzhen and Hangzhou, focused particularly on developing humanoids. A few weeks ago, a viral story highlighted how a Bay Area startup can spend two weeks getting quotes from US suppliers. The same startup received three detailed quotes from Chinese suppliers in twelve hours.

This speed compounds: over a few short years, this advantage becomes structural, showing up in greater hardware cost reductions, capability improvements, and much faster iteration cycles.

We are conscious of this speed risk for European companies. The regulatory environment in Europe leans toward caution, often moving safety-first rather than move-fast-and-iterate (as we have seen with foundational AI).

This is not necessarily bad: robust safety standards can become a competitive advantage if companies build them into their products from the start – and in certain cases, a push for safety can accelerate automation and robotic deployment in key sectors.

However, speed really matters. Companies that get held back by overly-cautious policy or wait for perfect clarity in regulations will be second-movers in a market where real-world deployment speed is essential. Companies that can deploy at scale in the next few years will build irreplaceable proprietary data advantages. Potential workarounds include focusing initial deployments in human-free environments, much as autonomous vehicles were first trialled on closed test tracks. (For more on safety, including ISO 10218, see discussions here and here).

Going forward, we believe European startups can move fast and win by combining an outstanding supply of talent from the European robotics ecosystem, manufacturing excellence through deep relationships with component suppliers, and rapid deployment in adjacent customer environments. The playbook is not to beat China on commodity hardware cost or the US on cutting-edge AI models. It is to own the customer, the deployment, and the data, and to be faster at getting robots onto factory floors and into assembly plants.

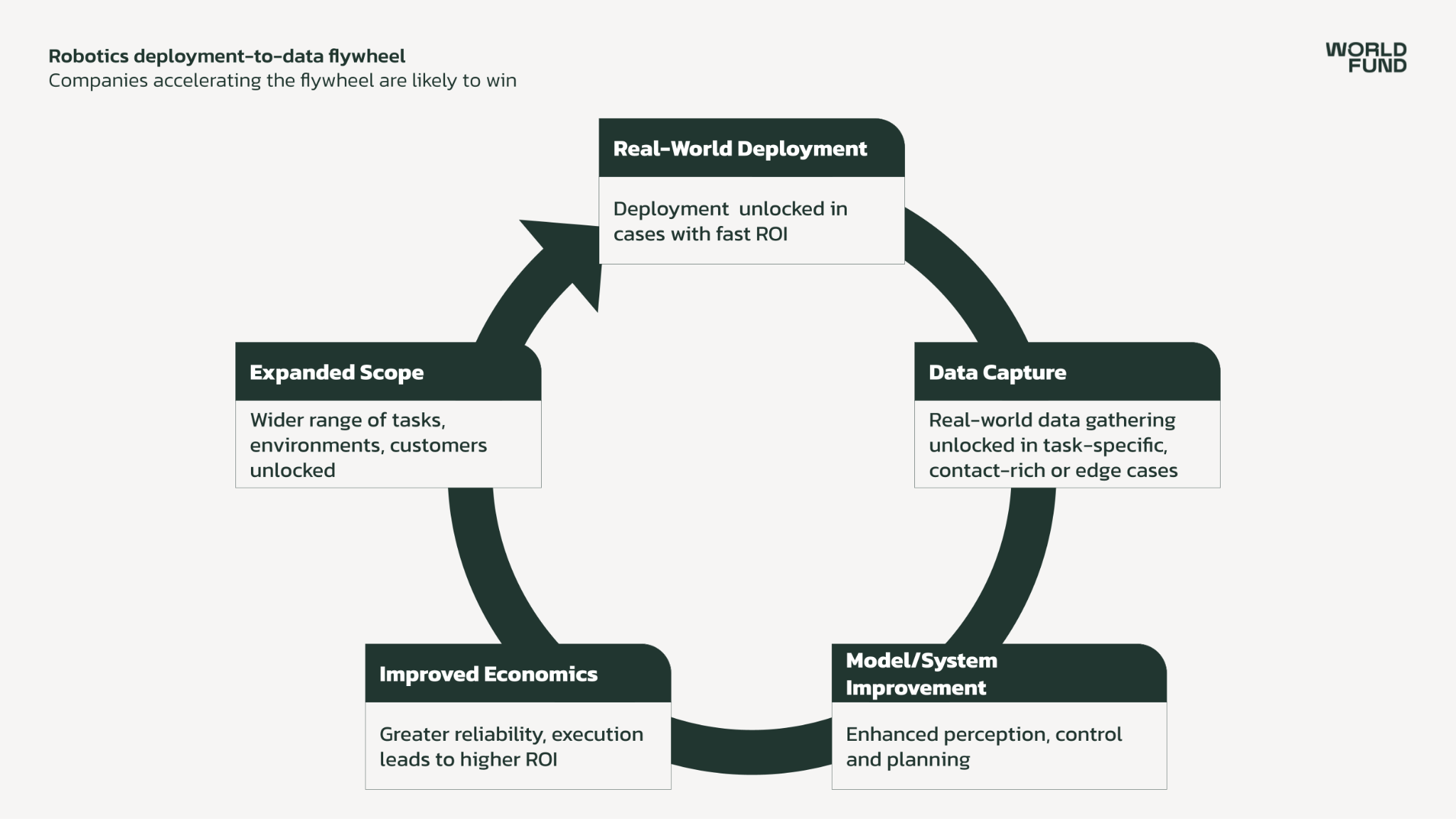

Winning companies spin the deployment-to-data flywheel

After studying the ecosystem, we noticed that several characteristics appear across the startups gaining strong traction.

First, they start narrow. The robots do one boring-but-essential task well: palletising boxes, moving material, and automating excavation. From this narrow foundation, companies expand gradually, the opposite of the over-hyped general-purpose robot pitch that promises to replace humans across countless tasks. A narrow initial focus enables faster learning, clearer ROI, and a path to scale within a specific sector before attempting to generalise.

Second, they obsess over the total cost of ownership and implementation, rather than just the cost of components. They choose hardware thoughtfully, without racing to the bottom on CapEx. Instead, they minimise the entire ownership stack: good hardware, exceptional implementation, intuitive software, and forward-deployed engineers with a strong understanding of the teams using robots on the ground. Finding the right business models and integration approaches allows companies to plan for customer relevance and long-term scaling – and can be a source of significant competitive advantage. A robot that is internally designed and built, runs reliably and requires far less integration time and operational overhead will win every time.

Third, they own the data generated during deployment. The robots gathering real-world data belong to the company, not the customer – exemplified by increasing adoption of RaaS models. Customers accept this because they still get a strong solution without worrying about the trickier aspects of deployment. This data ownership enables continuous improvement: the robots in the field effectively become a training fleet. Rivals without deployment at scale simply cannot learn as fast, even if their lab prototypes are technically comparable.

Finally, they are able to bring all of these together to spin the real-world deployment-to-data flywheel. They move robots from the lab to customers as fast as possible, even if imperfect. Every deployment generates data; every hour of real-world operation surfaces failure modes that sim-to-real or YouTube-based training cannot catch. This feeds back into the product, improving reliability, reducing downtime, and expanding capabilities. The fastest companies complete this cycle months ahead of peers. (For more, check out this piece at NotBoring.)

Altogether, we believe these strategies will be the source of differentiation for winning European robotics startups.

Where we see the greatest opportunities: boring tasks, big markets, real emissions reductions

At World Fund, we are interested in founders and startups that are developing an economically compelling use case in a global market, enabling significant decarbonisation impact, and have a clear business model that follows the strategies above.

The end-use sectors we are most focused on are those facing acute labour constraints, which contribute significantly to greenhouse gas emissions, and are essential to European resilience. Energy infrastructure – particularly grid modernisation and renewable energy deployment – faces a severe shortage of skilled trades. Construction is the world's least productive major sector, and the labour turnover is brutal: workers often leave after mere months. Manufacturing across Europe is rebuilding competitiveness as supply chains fragment. Agriculture has real labour shortages and requires robotics solutions with extreme specialisation (a robot that harvests raspberries struggles to pivot to potatoes).

These are also the sectors where the climate case is often most compelling. Robots can help increase process efficiencies and yields, reduce energy consumption or unlock faster deployment of key clean energy technologies, accelerating a pathway to net zero.

We are looking for companies that ideally target one of these sectors. They start with a boring, high-ROI use case, and are building business models to turn each deployment into a learning opportunity through the “deployment-to-data flywheel”.

If you are building robotics solutions in energy, construction, manufacturing, or agriculture – especially if you are targeting the European market with a team that understands both the customer and the deployment requirements – please get in touch at robin@worldfund.vc.

.webp)

.svg)