.svg)

.svg)

Geologic hydrogen: A new primary energy source?

Earth’s hidden hydrogen: Could geological reserves unlock a clean energy revolution?

In this article, we explore the emergence of geological hydrogen, a potential resource hiding beneath our feet. We examine the science and the economics of this space, and identify companies racing to unlock what could be the first new primary energy source in nearly a century.

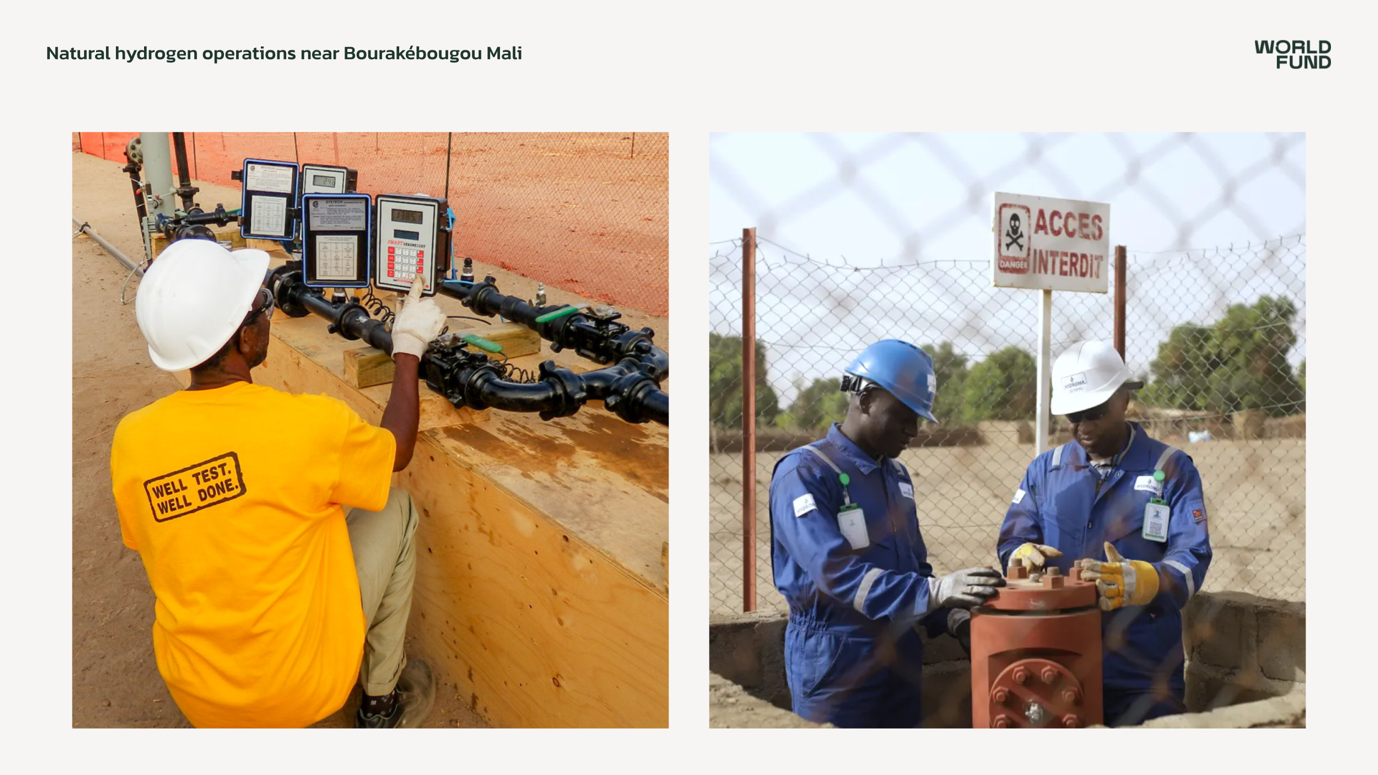

The village that runs on geologic hydrogen

In a small village in Mali, a well has been producing natural hydrogen for over a decade. The well, first drilled in 1987 near the village of Bourakébougou in search of water, was quickly plugged after an unexpected gas explosion. It remained closed for 25 years and was not re-tapped for hydrogen production until 2012. The site is now producing 98% pure hydrogen that powers the village at an estimated cost of around €0.50 per kg of hydrogen. That figure alone is remarkable, as it undercuts every hydrogen production method on the market today, including from fossil fuels.

Hydroma, the company that developed the site, went on to drill 24 wells within ten kilometres of the original discovery between 2017 and 2019. These wells identified five stacked reservoirs at depths ranging from 100 to 1,500m. The estimated reserves total 670 Bcf of hydrogen, approximately 2 Mt or 6 TWh - roughly equivalent to the annual electrical energy consumption of Munich.

Although the scale of this site is small, it raises the question of whether this resource could exist elsewhere at a far greater scale.

What is geological hydrogen?

Geological hydrogen refers to molecular hydrogen that is naturally generated and stored within the Earth’s crust through ongoing geochemical processes, rather than produced from fossil fuels or water electrolysis. A number of “colours” are associated with this type of hydrogen. “Gold” often refers to geologic hydrogen, while “white” and “orange” refer to its two subcategories: natural (white) and stimulated (orange) hydrogen.

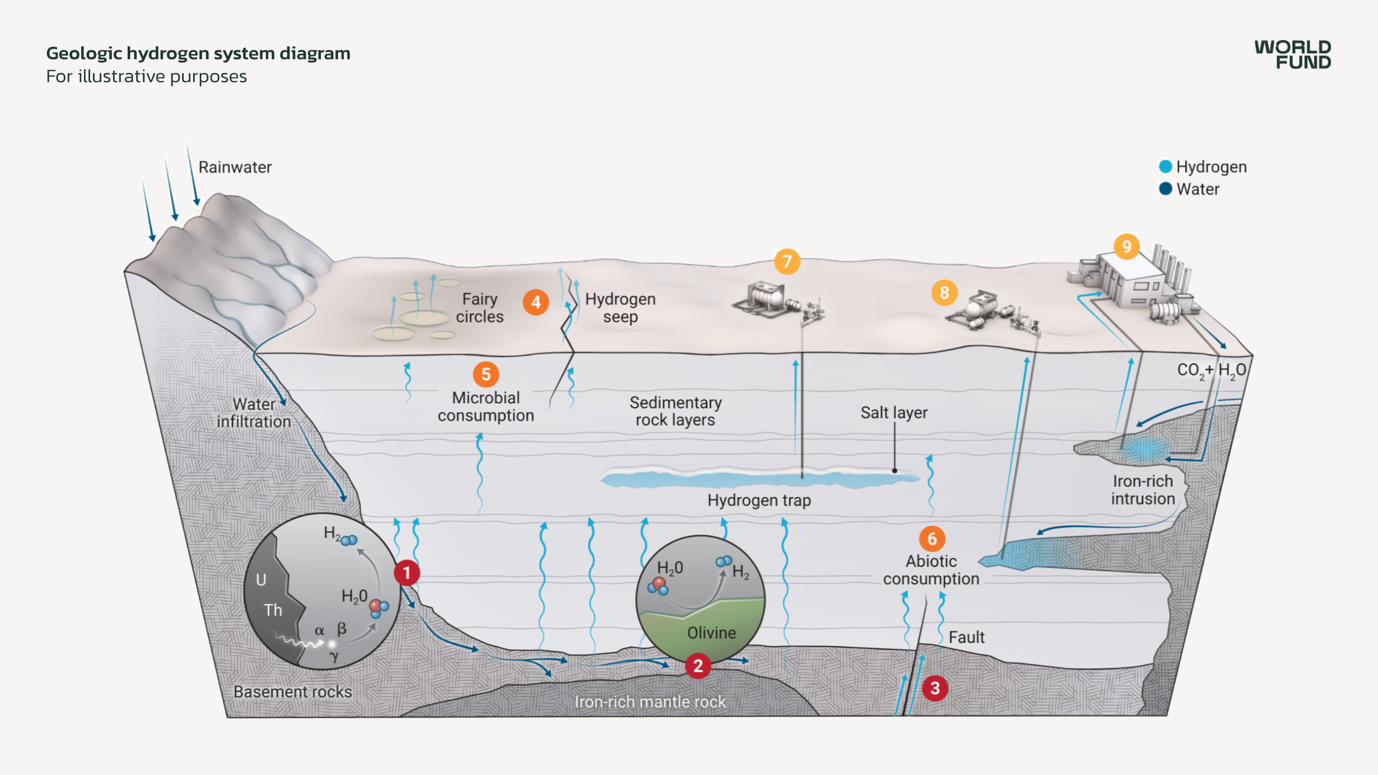

Natural hydrogen is formed primarily through a process called serpentinisation, in which iron-rich ultramafic rocks such as olivine react with water at elevated temperatures and pressures. The iron oxidises, and the water is reduced, yielding molecular hydrogen. This reaction is ongoing in the subsurface, meaning that, unlike oil and gas, which were generated over millions of years and exist as "fixed" reserves, geological hydrogen is continuously produced on much shorter time scales.

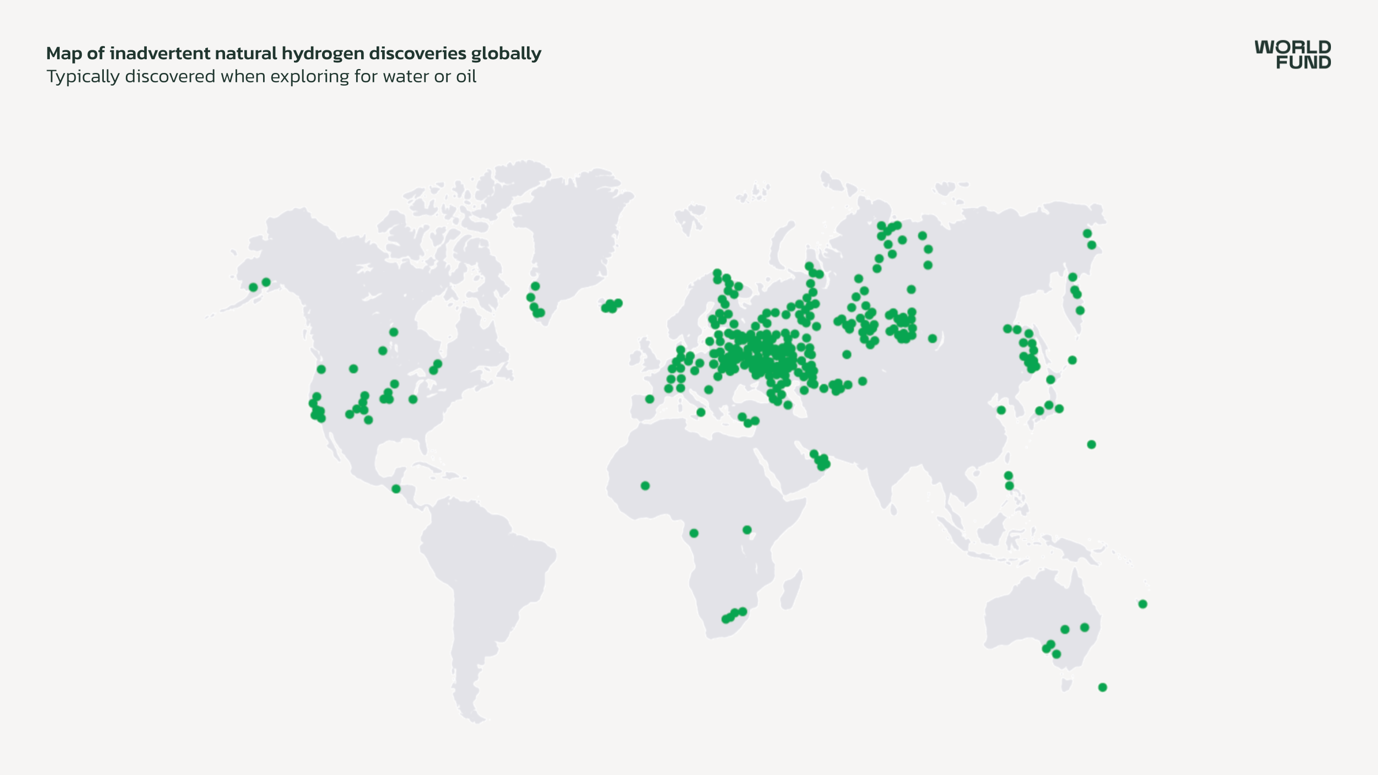

Surface observations of hydrogen are globally ubiquitous in soils, ocean vents, and deep boreholes, and regional fluxes can exceed thousands of cubic metres per day. Notable outgassings include Chimaera, Turkey, where flames from hydrogen (and methane) have been burning for millennia. More recently, even larger hydrogen outgassing fluxes have been identified at a chromium mine in Albania and in the Philippines, where a source is releasing 18x more hydrogen than the Mali system.

For commercial extraction to be viable, however, this hydrogen needs suitable geological formations to trap and accumulate it - much like a conventional gas reservoir.

The second pathway is stimulated, or “orange,” hydrogen. Here, water is injected into iron-rich rock formations, often with a catalyst, to trigger and accelerate the serpentinisation reaction in a controlled manner. Although potentially costlier than extracting naturally accumulated hydrogen, stimulated production increases the range of potential production areas and significantly reduces exploration risk as suitable iron-rich rock bodies are well characterised, easy to find, and widely distributed.

Hydrogen, an emissions heavy industry

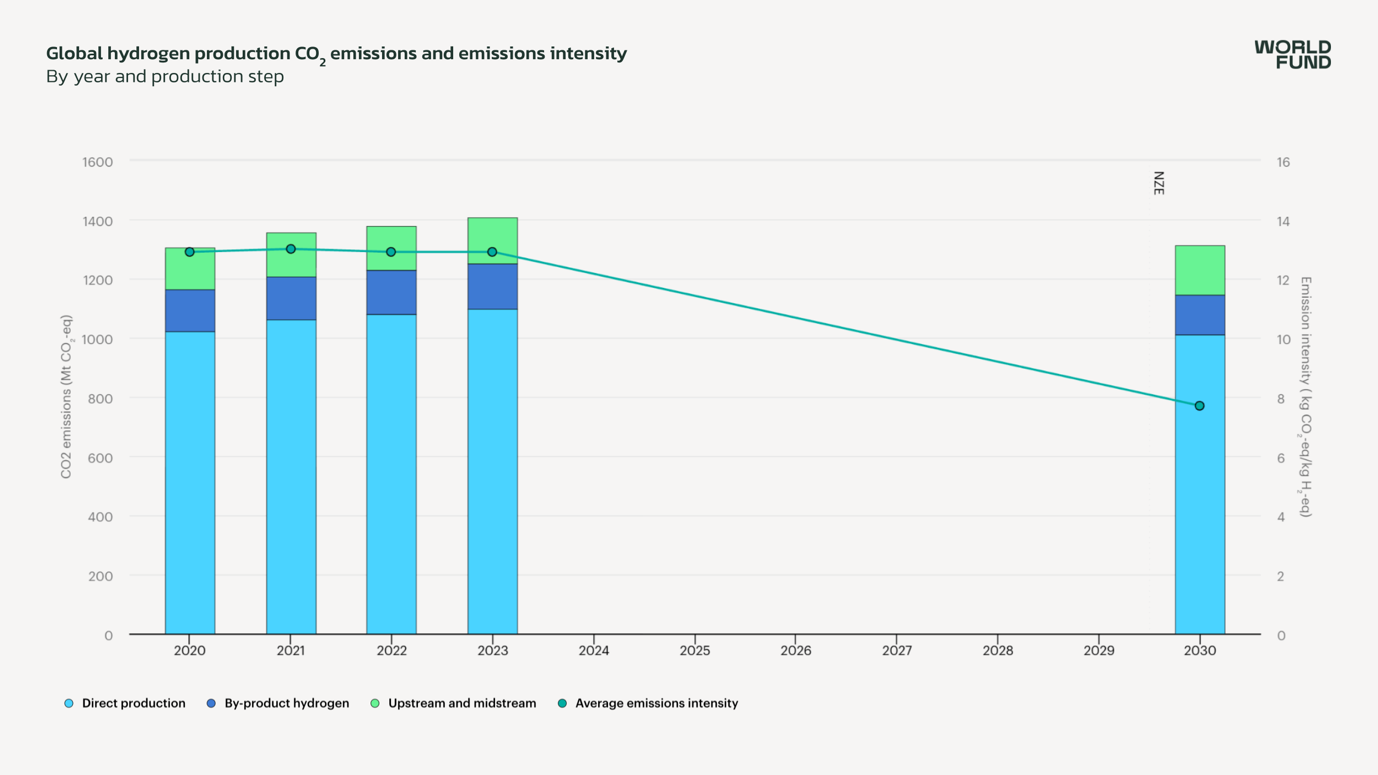

Global hydrogen consumption reached 100 Mt in 2025, with approximately half of demand coming from ammonia and methanol production, and oil refining accounting for the rest.

Although hydrogen has seen quite the hype cycle in recent years, the existing demand is enormous and emissions heavy. Unabated fossil fuels dominate the hydrogen supply chain, with nearly two-thirds of production coming from natural gas reforming and the rest largely from coal gasification concentrated in China and India. Low-emissions hydrogen accounts for just 1% of total production.

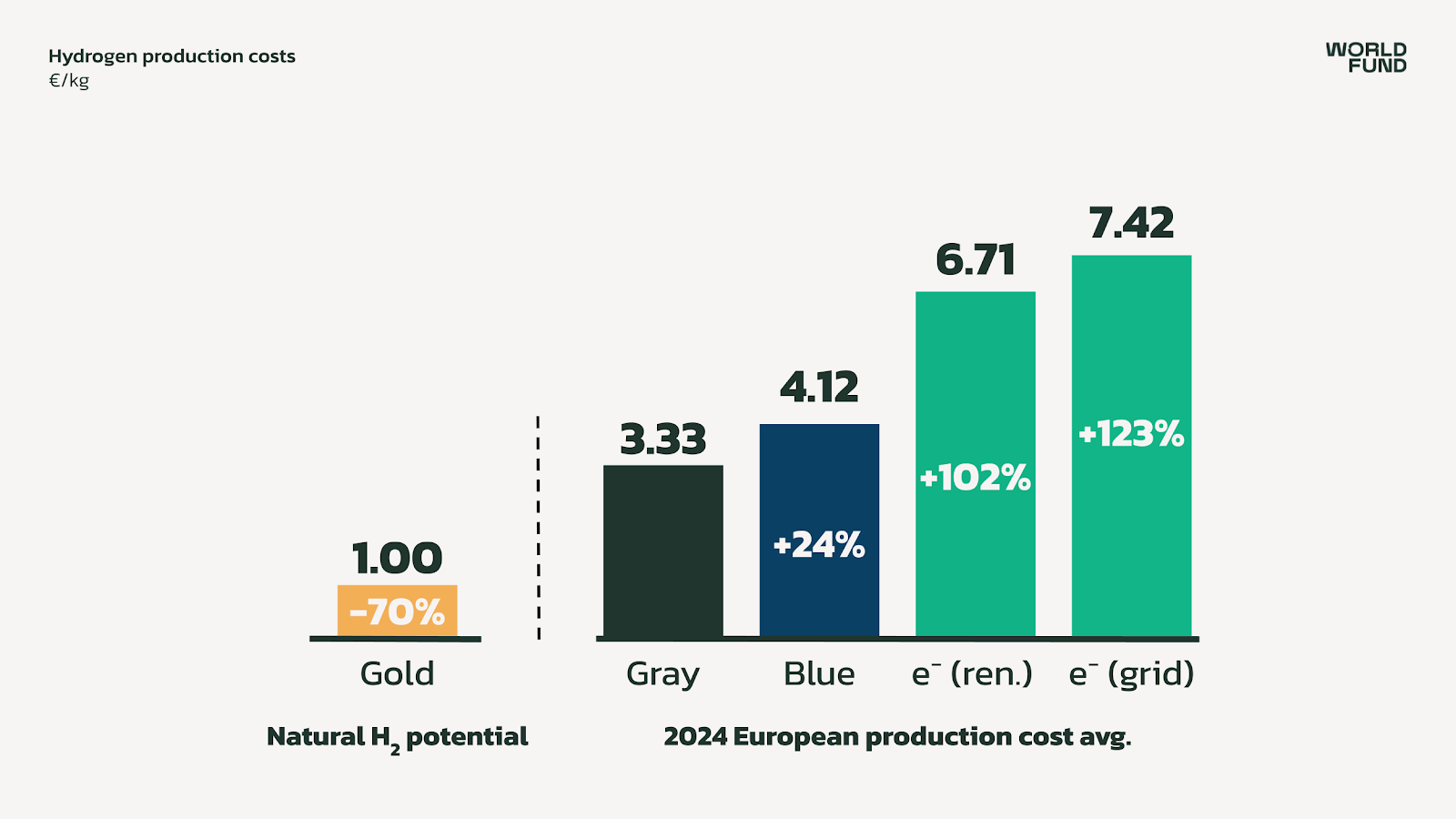

The climate implications are severe as hydrogen production currently generates approximately 1.4 Gt of CO₂ annually with an average emissions intensity of 13 kg CO₂ per kg H₂. Natural hydrogen could realistically achieve an intensity of less than 1 kg CO₂ per kg H₂, representing a reduction of over 90%.

The economics are equally compelling. In Europe in 2024, grey hydrogen from natural gas reforming had an average production cost of €3.33 per kilogram. Blue hydrogen commanded a 24% premium at €4.12 per kilogram while green hydrogen averaged around €7.00 per kg.

By contrast, natural hydrogen has a credible pathway to production costs of around €1 per kilogram, roughly 70% cheaper than today’s grey hydrogen.

No other low-carbon hydrogen pathway comes anywhere close on cost.

Beyond replacing existing dirty production, natural hydrogen’s lower costs could also make currently uneconomical hydrogen use cases viable. For example, it could help make synthetic fuels and high temperature industrial heating a reality.

Why hasn’t anyone ever utilised Earth’s natural hydrogen reserves?

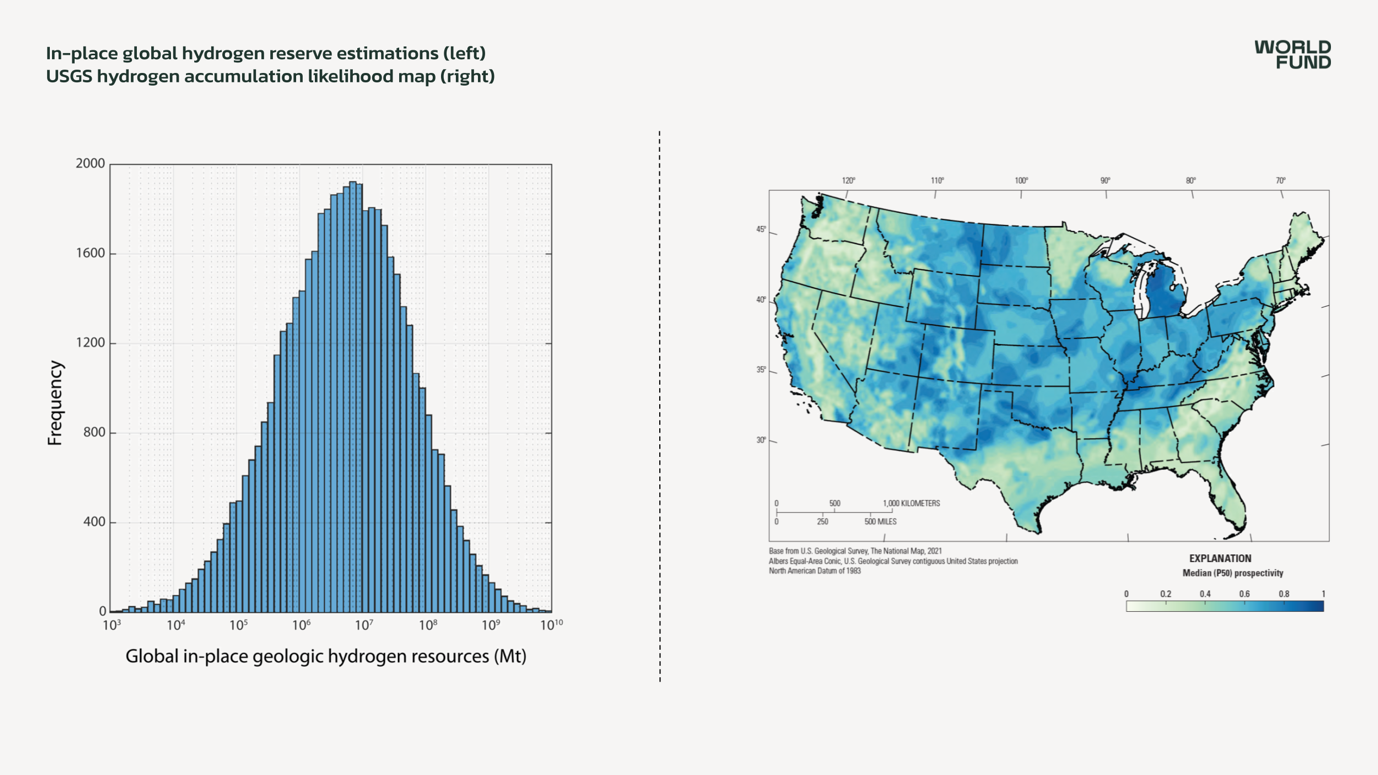

Academic work suggests that around 5.6 million Mt of hydrogen could be present in the subsurface. Assuming just a 2% recovery rate and current consumption rates, this could satisfy demand for the next 1,000 years. This 2% recovery alone would contain more energy than all proven natural gas reserves on Earth.

Further studies indicate that there is also potentially a 23Mt of total hydrogen flow escaping the Earth’s surface annually from geologic sources.

So, if geological hydrogen is so abundant and so cheap, why has no one commercially exploited it at scale? In short, because until recently almost no-one has been looking for it.

Approximately 20 wells have been drilled globally with the specific aim of finding natural hydrogen, compared to the millions drilled for oil and gas. Historically, geoscientists had also assumed that accumulations were probably unable to form because hydrogen is highly diffusive and highly reactive through both biotic and abiotic processes. Additionally, only a handful of oil and gas fields have ever reported hydrogen concentrations above 1%, largely because the geological settings where hydrogen is most likely to occur are not where hydrocarbons are found.

Yet high concentrations are now being found.

HyTerra, an Australian-listed company exploring in Kansas, recorded hydrogen readings of up to 96% and helium up to 5% in mud gas samples during its 2025 drilling campaign along the Nemaha Ridge. Other players, such as Gold Hydrogen, have also found high concentrations, recording 95% pure hydrogen during well testing in South Australia.

It is becoming clear that finding high concentrations of hydrogen is increasingly possible, but no one has yet demonstrated commercially viable flowing volumes from a purpose-drilled well. Existing subsurface models built for hydrocarbons are not useful predictors for hydrogen accumulations, and thus, new models, new data, and more wells are needed. Analogues have been drawn to the shale boom of the 1990s and 2000s, where it took multiple decades for the technology (horizontal drilling and hydraulic fracturing) to mature sufficiently to economically extract the resource.

The race is on

What was an academic curiosity just five years ago is now a funded, competitive industry.

Over 40 companies, public and private, are actively searching for geologic hydrogen, up from just ten in 2020.

In the United States, Koloma stands out as the best-capitalised pure-play natural hydrogen company, having raised over $350m with recent expansion to explore in the Philippines. HyTerra continues its drilling programme along the Nemaha Ridge in Kansas, building a proprietary geological model that has now been validated by its McCoy 1 well.

In Australia, Gold Hydrogen is advancing its programme on the Yorke Peninsula in South Australia, while in Canada, MAX Power Mining Corp has recently received the first-ever Canadian drilling licence and QIMC has recently completed a 711m discovery hole. Even China is getting in on the action, spudding its first well in late 2025 near Xilinhot in Inner Mongolia.

On the stimulated hydrogen side, Dr. Alexis Templeton completed the first successful field test of stimulated hydrogen production in Oman, a world-first validation that the serpentinisation reaction can be triggered and sustained in real-world subsurface conditions. Meanwhile, Vema is working on its first stimulated hydrogen well in Quebec, with the drilling of the first two pilot wells recently completed.

The World Fund perspective

At World Fund, we are watching this space closely. We see the enormous potential, but the commercial breakthrough moment we are waiting for has not yet occurred. No company has demonstrated a clear path to economically viable, large-scale extraction of geological hydrogen.

What would change our view? For natural hydrogen, a discovery with demonstrated flow rates, not just high purity readings in mud gas, but sustained production from a purpose-drilled well (even if below commercial rates). To meaningfully de-risk exploration, we believe that further advancements in novel subsurface modelling, advanced geophysical imaging, and data analytics are critical for increasing the likelihood of finding viable accumulations.

For stimulated hydrogen, we are eager to see additional proof points around the alignment between lab-scale tests and models with real in-field results. Translating compelling reaction kinetics out of the lab and into the subsurface that demonstrate a realistic path towards competitive unit economics is key. Ultimately, for both production pathways, we want to see the speculative thesis mature into a convincing, data-supported commercial case.

Advances on either of these fronts could be a real paradigm shift in making geologic hydrogen a reality. This could be especially valuable for Europe, given the general lack of natural resources available. Geologic conditions for both natural and stimulated hydrogen exist across the continent, from the ophiolites of the Alps and Pyrenees to the ultramafic formations of Scandinavia. If viable in Europe, geological hydrogen could simultaneously address the trifecta of European policy priorities: energy security, industrial competitiveness, and decarbonisation.

We believe the shale analogy is instructive but sobering. If geological hydrogen follows a similar trajectory, broad commercialisation could still be decades away. Capital is now flowing, and we are beginning to see failures and successes happening with greater frequency. There are also significant efforts to expedite the commercialisation of geologic hydrogen, such as the Chimaera Fund of Renaissance Philanthropy. Their goal is to invest in open-access field demonstrations, so that natural hydrogen has a much quicker time to market than shale gas and geothermal, which came before it.

Geological hydrogen is by no means a guaranteed revolution, but the conditions are slowly assembling. Capital is being invested, interest is rising, and initial technical validation is being seen.

The next 12 to 18 months will be pivotal. Multiple exploration wells are being drilled across numerous continents, stimulated hydrogen results from new field tests are expected, and major oil and gas companies are watching. If a commercially viable accumulation is found or stimulation proves economically feasible, the trajectory of the entire hydrogen economy could shift.

If you are working in this space and are not yet on our radar, please get in touch at sebastian@worldfund.vc.

—

About Craig Douglas, Partner, World Fund

Craig Douglas is a Partner at World Fund. He has been investing in climate tech companies over the past 12 years at World Fund and SET Ventures, one of Europe’s longest-running climate funds. Craig has pioneered ESG and Impact in the venture community after creating a leading ESG framework in 2012 and co-designing a model that links impact to fund performance and compensation, now used by over 50 funds. Craig is also an advisor to the EU Commission on Energy.

About Mark Windeknecht, Principal, World Fund

Dr. Mark Windeknecht is a Principal at World Fund. He brings deep technical expertise to climate investing, with a background in energy systems and a doctorate in Electrical and Computer Engineering from the Technical University of Munich, where he also worked as a researcher. Prior to World Fund, Mark was at Vito One, investing across the PropTech, ConTech, and EnergyTech verticals. Mark serves as an advisory board member at portfolio companies cylib and aedifion, and as a board observer at IQM.

About Sebastian Lindner-Liaw, Investment Research Analyst, World Fund

Sebastian Lindner-Liaw is an Investment Research Analyst at World Fund, where he focuses on deep tech climate investments across energy and industry. He holds a background in engineering and earth sciences and has prior experience in electrifying mobility at Rivian, BMW, and Trek Bicycles.

.svg)