.svg)

.svg)

Electrofuels for aviation

The state of: electrofuels for aviation

Introduction

Synthetic fuels (or “electrofuels”) are often touted as the ultimate medium-term solution to decarbonising aviation. In this analysis, we will not only examine the potential impact of electrofuels within the aviation industry, but also the (potentially adverse) consequences of deploying them in the wider energy system. We will then dive deeper into existing processes for electrofuel production, as well as examining where innovation could occur. This briefing is divided into three parts:

Part I - Electrofuels for aviation

Part II - Electrofuels within the wider energy system

Part III - Processes, challenges, and innovations

Part I: Electrofuels for aviation

If we draw a box around the aviation industry and examine how to decarbonise it, there is only one sensible answer: drop-in fuels.

Global aviation traffic is forecast to double by 2040, and options for decarbonisation are limited.

Battery electric flight may displace some very short, low volume flights, but 81% of emissions from aviation occur from medium and long haul flight.

Meanwhile, we do not expect hydrogen-powered aircraft to be operational at scale by 2040. This is because

- Using hydrogen in planes would require extensively redesigning the aircraft, due to hydrogen’s low energy density (volumetric). The regulation and certification of new aircraft is complex, expensive and time consuming.

- We do not anticipate that the refuelling infrastructure and logistical challenges of using hydrogen will be resolved quickly enough to lead to any early retirement of aircraft in today’s fleet. We therefore do not believe that hydrogen aircraft will comprise a significant proportion of flights in 2040.

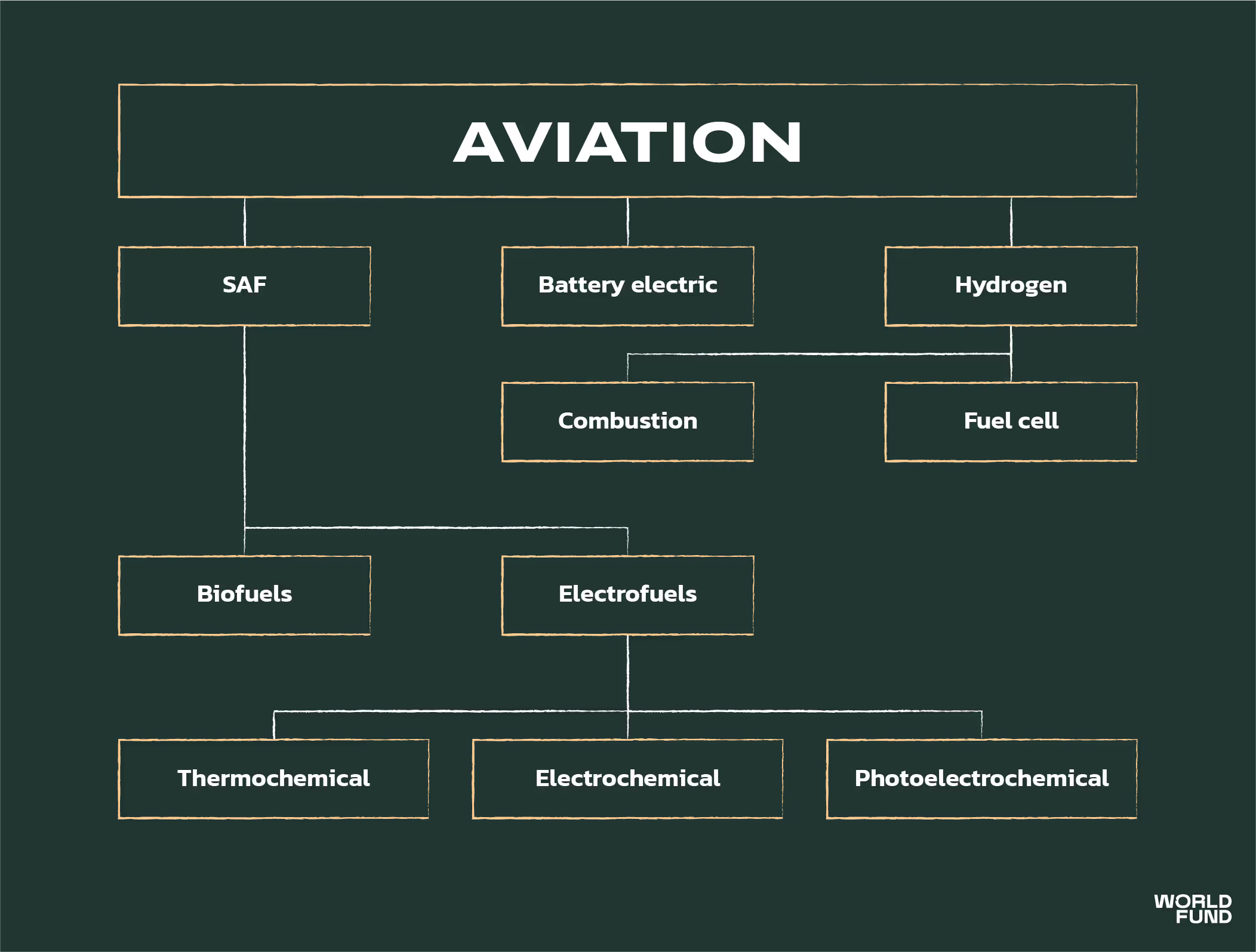

Thus, if aviation is to be significantly decarbonised by 2040, it is necessary that drop-in Sustainable Aviation Fuel (SAF) for current planes must play a leading role.

BIOFUELS VS ELECTROFUELS (E-FUELS)

There are two types of SAF. Both take a source of carbon, and convert into a hydrocarbon fuel. Biofuels use carbon from plants and organic matter, whilst electrofuels (“e-fuels”) aim to use CO2 from a non-biogenic source, such as Direct Air Capture (DAC).

Of the 100 million litres of SAF produced in 2021, over 99% was biofuel. The production of biofuel is currently significantly more mature and cost effective than producing e-fuels. However, whilst biokerosene production will increase in the future, capacity is limited. This is simply due to the limited availability of sustainable biomass, which will become increasingly constrained as biomass becomes a major feedstock for chemicals, plastics, and BECCS.

It is well accepted that both biofuels and e-fuels will play a major role in future SAF production. In this report, we focus purely on the investment opportunities and challenges of e-fuels.

Part II - Electrofuels in the wider energy system

It is often the case that the aviation industry is evaluated in isolation, and thus, electrofuels emerge as the obvious solution. However, it’s crucial to also evaluate the impact of electrofuels on the wider energy system.

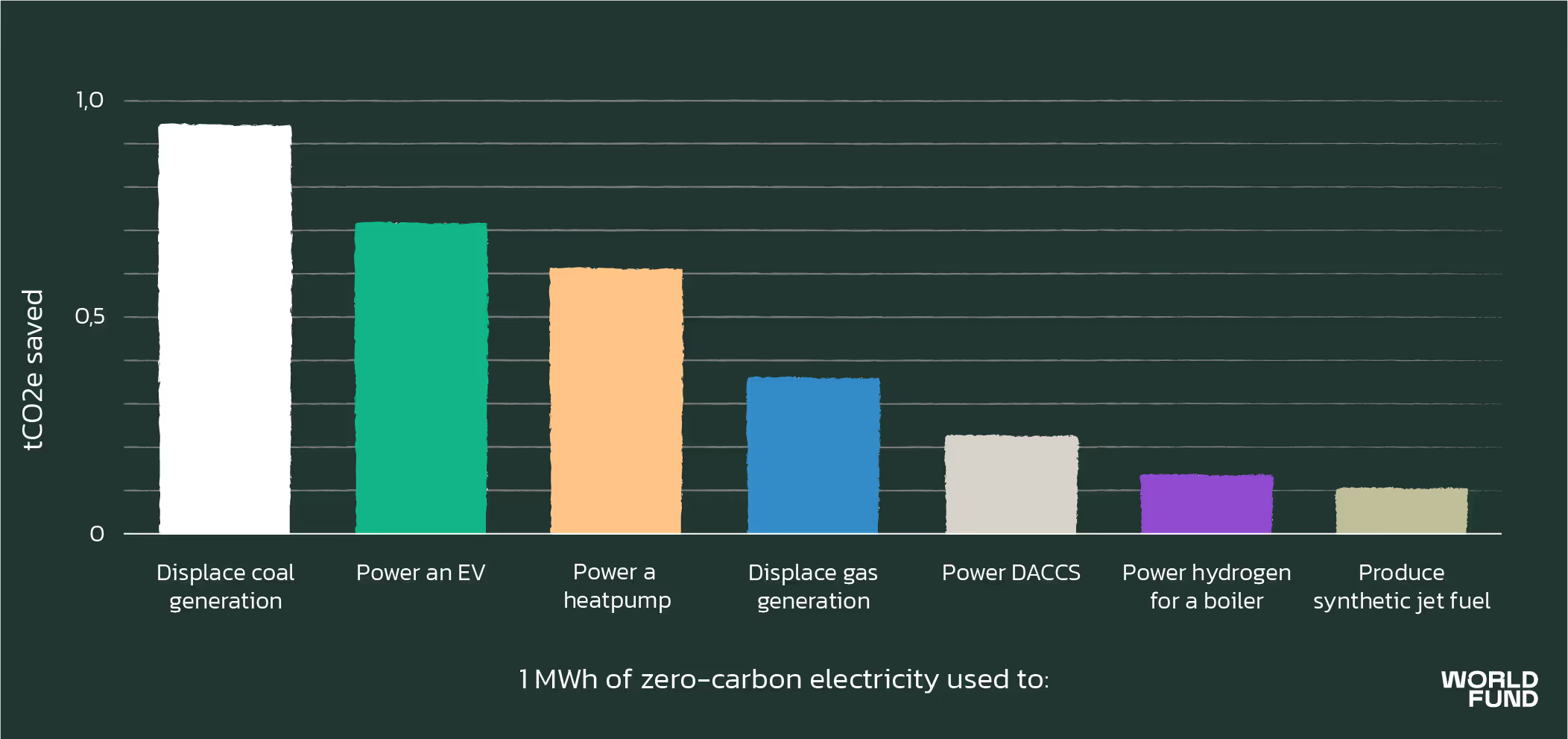

The best KPI to evaluate this is the CO2 saved per MWh of renewable electricity. Ie, does it make sense to use our renewable energy resources to be making synfuels, compared to, for example, displacing gas generation or powering a heat pump?

Before we start, it’s important to first understand three things:

- Burning synfuel still emits CO2. Note that all synthetic fuels still emit CO2 when burned in a jet engine. The difference is that the carbon used to make the fuel comes from the atmosphere, not the ground, thus theoretically making the fuel “carbon neutral”.

- CO2 is only part of aviation’s emissions. When kerosene is burnt in a jet engine, it also leaves vapour trails (“contrails”) in the sky, which also contribute to warming of the earth. We actually still don’t know exactly how much warming they contribute, but we think that it’s at least double that caused by CO2 emissions from planes.

- Making electrofuels uses a lot of (renewable) electricity. You need electricity for three main things:

- Producing green hydrogen (“electrolysis”)

- Producing CO2 - using Direct Air Capture (DAC)

- Powering the fuel-production process

Out of these, the energy for producing green hydrogen is usually the biggest.

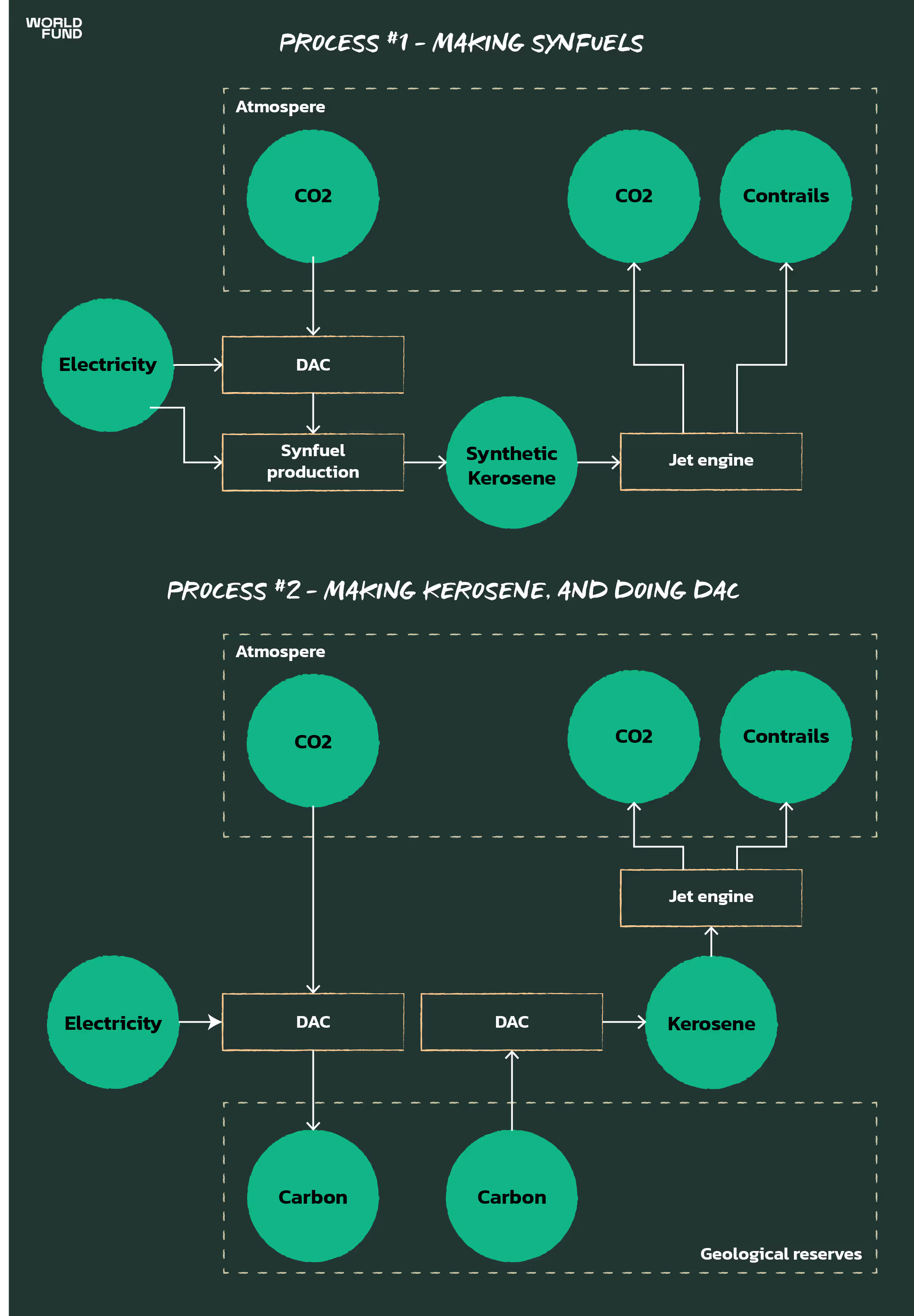

Now let’s take a look at how carbon/CO2 moves around when we make electrofuels vs when we make kerosene. We’ll consider two scenarios:

#1 - Making synfuels

#2 - Making kerosene, and using Direct Air Capture to capture the CO2 emitted.

The important thing to note here is that both processes require Direct Air Capture (see our later section for reasons why other CO2 sources for synfuels are not scalable or sustainable). Thus, both methods require a large amount of renewable electricity.

However, the synfuels process requires a lot more renewable electricity, because producing green hydrogen is extremely energy intensive. You would have to at least double the renewable electricity needed for kerosene-and-DAC to have enough to make synfuels. The problem here is that this renewable electricity is badly needed in other places. Scaling up the production of synfuels would prevent vast quantities of renewable electricity generation being used for things that can save much more CO2 per MWh of electricity. This figure by the UK’s Committee on Climate Change illustrates ballpark figures:

Despite this, there are some reasons why it still may be better to use synfuels. for example:

- Using synfuels reduces the formation of contrails, since the fuel burns “cleaner”. We know the reduction here is significant, but the science is still not clear on the expected amount.

- The production of oil for kerosene generates emissions, predominantly from methane leaks. This is highly dependent on the geography and extraction methods used.

Further discussion of these tradeoffs can be found in Appendix B.

CONCLUSION OF PART II

It is possible that electrofuel production may produce an adverse climate effect compared to a scenario in which DAC is used to compensate for emissions from kerosene. To determine this would require advances in our knowledge of:

- The warming effects of contrails in general

- The reduction in contrails possible form using electrofuels (likely significant)

- The reduction in aromatics content possible in existing kerosene refineries

- The embodied emissions incurred in producing kerosene in future oil markets

- Required energy (and associated renewables opportunity cost) of CO2 sequestration

We expect to gain better clarity on several of these issues within the next few years - for example from MIT and Delta Airline’s recently announced study on contrails.

On balance of probability, we find it likely that electrofuels have a beneficial climate impact beyond using regular kerosene with DAC - however, if present, this benefit may be very limited. The Royal Society confirms that further research is needed here to evaluate the overall lifecycle climate benefit of synthetic fuels.

If electrofuels do turn out to be beneficial, part III analyses the current state of the space, and future opportunities.

Part III - Processes, challenges, and innovations

This part examines the electrofuel tech stack, and future opportunities for improvements/breakthroughs.

ESTABLISHED PROCESSES

There are three types of processes that can create electrofuels: thermochemical, electrochemical and photoelectrochemical.

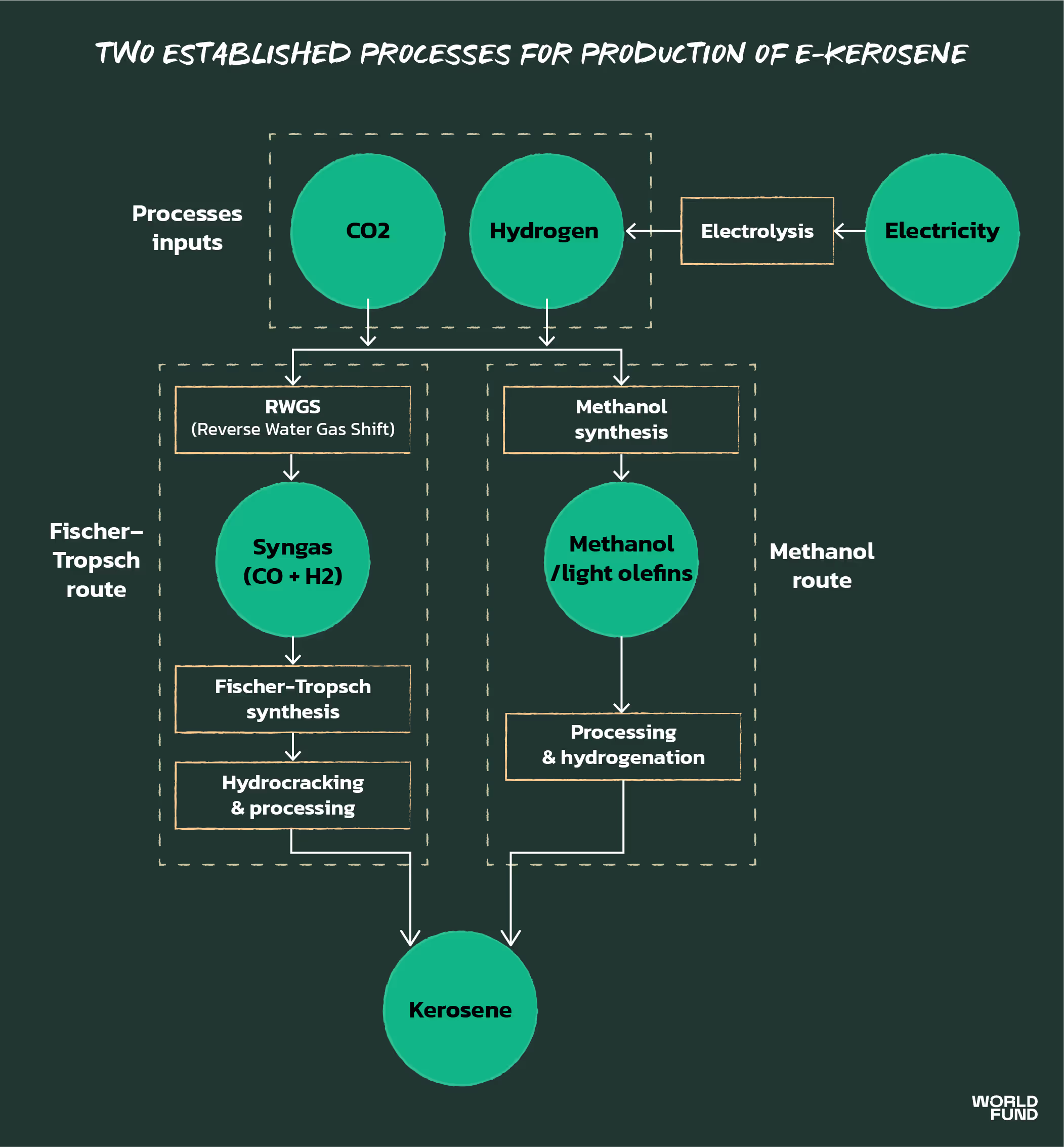

Today’s well established processes are mostly thermochemical, and build on well-explored reactions and processes for producing hydrocarbons. In particular, there are two largely thermochemical production pathways that are the most mature: Fischer-Tropsch synthesis, and methanol synthesis.

Note that the energy efficiency of both pathways is roughly the same.

Fischer-Tropsch pathway

The Fischer-Tropsch process is well established, since it has been widely used since the 20th century to produce synthetic diesel, gasoline, and air fuel. In the past, however, syngas was produced from a fossil fuel source, such as the gasification of coal. Therefore, the part of the Fischer-Tropsch route least proven at scale is the “Reverse Water Gas Shift” (RWGS) reaction, which converts the CO2 (carbon dioxide) source into CO (carbon monoxide) in the form of syngas, which can then be used for Fischer-Tropsch synthesis. Upgrading the product of the Fischer-Tropsch process (synthetic crude) into jet fuel is a mature process, similar to that deployed at scale in crude oil refineries.

Methanol pathway

Whilst there is proven deployment of this pathway for producing gasoline and other hydrocarbon fuels, the methanol route is less mature for producing jet products. Therefore the last refining step of this pathway (turning methanol to distillate/kerosene) is the least proven.

It should also be noted that whilst the Fischer-Tropsch process has been certified by ASTM as a valid pathway for producing synthetic kerosene, as of 2022, the methanol pathway has not.

CHALLENGES

Many startups in the electrofuel space are focusing on improving one of these two pathways. What are the challenges they face?

Electricity requirement - scale

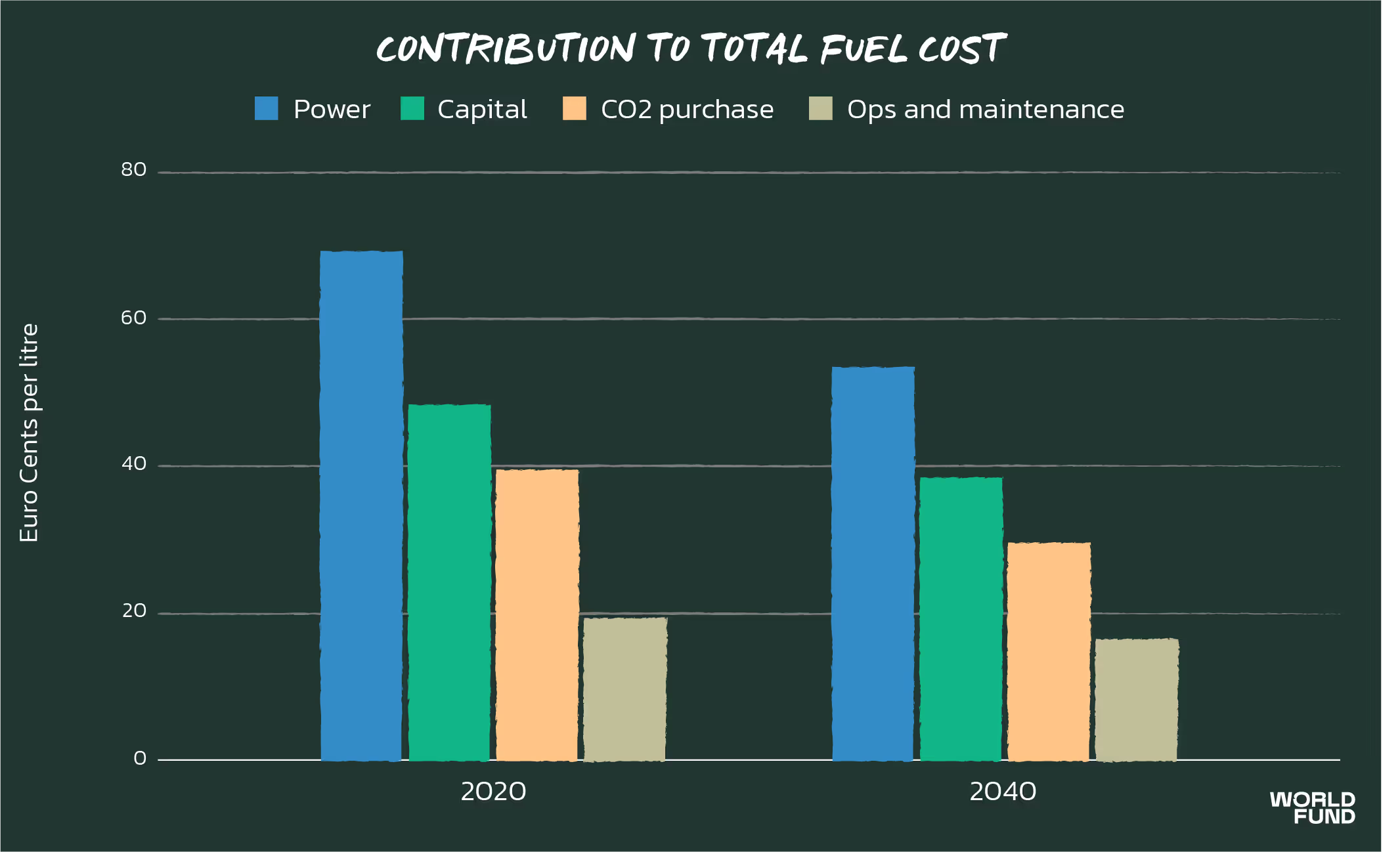

By far the largest factor limiting the production of electrofuels is their enormous electricity requirement. This is the primary reason that electrofuels currently cost at least 3x the price of conventional kerosene, and usually more. The scale of this barrier should not be underestimated.

Using current technologies to replace 8% of European aviation fuel with e-fuel in 2040 (8% is the minimum blend mandated by the EU for that year) would require roughly 140 TWh/yr of electricity. This is roughly equivalent to the entire electricity consumption of Sweden or the Netherlands.

The majority of electricity goes towards producing hydrogen through electrolysis (green hydrogen). Not only does power consumption dominate the levelised cost, but more than half of the upfront capital typically goes towards hydrogen electrolysers. Therefore, it is not uncommon for hydrogen production to make up 60% or more of the levelised cost of synthetic fuel.

This sensitivity to the cost of electricity means that market leaders in electrofuel production will likely have facilities located near the world’s most abundant renewable electricity resources.

Electricity requirement - intermittency

Due to the need to run on cheap renewable electricity, another challenge is the intermittency in energy supply. Hydrogen and CO2 can be produced and stored in advance, but running some chemical processes is challenging without an uninterrupted supply of energy. Thus, there is a challenge in building processes that can run efficiently at part-load, as well as ramp-up and ramp-down quickly.

There is also a financial obstacle here. If a plant needs to be operated for at least, say, 50% of the time to break even, then there will not be sufficient “excess” renewable power available from the grid to power the plant over the course of a year. Therefore, many electrofuel production plants may wish to build their own sources of renewables.

CO2 source

There are two ways of sourcing the CO2 required for production: existing point sources, or direct air capture (DAC).

Point sources

Existing industrial processes such as cement production or power generation are examples of point sources that produce CO2. Biogenic sources, such as CO2 from waste, are also in use by several projects. Once captured, CO2 from these processes can be used as a feedstock for synthetic fuels. However, there are logistical and sustainability barriers.

Fuels produced from point sources of CO2 are less sustainable than those made with CO2 from DAC. This is because DAC takes CO2 from the atmosphere to make the fuel (the CO2 is re-emitted once the synthetic fuel is burned, but no additional CO2 is added to the atmosphere). In contrast, using CO2 from point sources only creates CO2 savings if the CO2 would not have otherwise been captured. This will become rarer in the coming decades, and thus the “carbon neutrality” of e-fuels made with CO2 from point sources will become increasingly questionable. Biogenic sources of CO2 cannot scale to large production volumes of electrofuels for the same reason (sustainable biomass availability) that hinders biofuels’ scalability.

Additionally, given the need for a production plant to be located in places of abundant solar or wind potential, many ideal plant locations are remote. Piping large quantities of CO2 to these locations would require significant infrastructure investments.

Direct Air Capture

Extracting CO2 from the air requires a lot more energy than extracting it from a point source, since CO2 is less abundant in the air. Therefore, using direct air capture requires significantly more energy, which substantially reduces the process efficiency.

For a Fischer-Tropsch pathway using high-temperature electrolysis, expected efficiencies would be in the order of:

Market dynamics

Demand for electrofuels

Electrofuels will not be cost competitive with conventional kerosene by 2030, and this will likely be the case for many years beyond. However, the market for synthetic fuels will nonetheless be made by policy-mandated blending of SAF into fuels. The EU’s “Fit for 55” policy package proposes the following binding blends:

Given the looming need to secure sufficient supplies of SAF to meet these requirements, airlines are already signing medium-volume (hundreds of millions of litres annually) offtake agreements for e-fuels with companies such as Velocys and HIF.

We see the possibility that the same advance-market-commitment playbook used by Frontier for carbon removal could be replicated in the e-fuel space.

It should also be noted that new chemical processes developed in this field (particularly electrochemical breakthroughs) often have applicability in producing sustainable hydrocarbon feedstocks for chemical production. Thus, the potential for technology transfer to the wider chemicals industry is high.

Market positioning

See Appendix A for a market map of the electrofuel space.

Broadly, there are two types of startups in the space: technology providers, and integrators. Technology providers sell products, expertise and engineering for a specific process step, whilst integrators combine processes to build a complete production pathway - sometimes purchasing off-the-shelf solutions from technology providers, sometimes building all processes themselves.

Examples of technology providers are INERATEC, who specialise in modular Fischer-Tropsch reactors, and Sunfire, who produce novel high-temperature co-electrolysers. There are also broader technology providers who do not focus purely on electrofuels, such as DAC companies or conventional low-temperature hydrogen electrolyser providers.

Integrators, such as norsk e-fuel and Arcadia eFuels combine technology solutions, secure funding, and build production plants.

Note that there are also a considerable number of exceptions, who as well as possessing a novel technology, choose to integrate or build an entire production process themselves. A notable example is Prometheus Fuels, which after raising its series B at a $1.5b valuation, is aiming to deploy several novel catalysts and materials in an ethanol-based production pathway. Despite being well capitalised, the energy requirements of its processes mean that it is likely to significantly miss its cost milestones for production.

It’s worth noting that historically, comparable chemical plants (such as coal liquefaction plants) typically require multi-billion capital investments in order to produce fuels at any meaningful scale (in the order of thousands of barrels per day). This is unlikely to change, and thus there are serious questions about how feasible it is for startups to out-compete existing energy & process engineering companies as “integrators”.

RECOMMENDATIONS

With this context in mind, where do interesting startup investment opportunities lie?

Uninteresting opportunities

New “integrator” companies combining well-established processes to make a traditional production pathway, such as the Fischer-Tropsch route, is not unique or defensible. Efficiency gains from integrating processes (for example, recycling waste heat from Fischer-Tropsch synthesis and using it for other process steps) are obvious improvements and not a sufficient USP. Large energy and chemical companies with decades of experience in process engineering can easily out-compete startups here.

Interesting opportunities

Individual process step improvements

The development/selling/licensing of novel solutions for individual process steps is a model better suited for startups, being inherently more capital-light. Licensing is already common in the field of catalysts. Some examples of individual process step improvements could be:

- Advances in high-temperature (SOEC) electrolysers, such as reducing their degradation, improving manufacturing costs, and developing generation of pressurised hydrogen

- Advances in catalysts, not only with higher efficiencies, but also with higher selectivities. Often only 50-60% of the hydrocarbons produced in a synthesis process are suitable for jet fuel, and whilst others (such as gasoline) can be sold, their revenue potential is lower.

- Advances in the Reverse-Water-Gas-Shift (RWGS) reaction, which remains at a lower TRL than the rest of the Fischer-Tropsch pathway

Electrochemical processes & electrocatalysis

Many researchers expect that the “next frontier” in e-fuels will arise from developments in electrocatalysis, which have accelerated in the past few years. Breakthroughs in this field could lead to new ways to produce synthetic fuels with precise selectivities, higher efficiencies, and cheaper reactors.

Advancements may arise from replacing individual process steps (eg electrochemical reduction of CO2 to CO/syngas, which is already being commercialised by Topsoe and Sunfire), or by the direct conversion of CO2 to fuels in one step. This single-step conversion of CO2 to fuels/long-chain hydrocarbons is considered by some to be a holy grail, and is currently a hot topic in academia. In theory it is possible, and expertise in the area is growing, but as of 2022 it has not yet been demonstrated.

Photoelectrochemical processes (“solar fuels”)

Solar fuels use sunlight to electrolyse hydrogen from water directly - without producing electricity first. There is wide academic interest here, and Synhelion, a spinoff from ETH Zurich, has begun construction of a pilot plant in Germany in an attempt to commercialise the technology.

Currently, costs of the photocatalytic devices remain high (they are largely based on noble metal catalysts), and efficiencies remain low.

CAPABILITY TO RUN INTERMITTENTLY

Established thermochemical pathways are yet to be operated at scale using intermittent electricity inputs. Projects that can demonstrate:

- The ability to ramp-up and ramp-down in minutes rather than hours

- The ability to run at part load

- A sufficiently low CapEx/OpEx ratio to be economically competitive running at reduced capacity factor

are of interest.

NOVEL SYSTEM INTEGRATION / ARBITRAGE OPPORTUNITIES

As previously stated, the production of hydrogen currently comprises the majority of e-fuel production costs. Additionally, in the coming decades, there will be a significant increase in the utilisation of hydrogen, CO2, and renewable energy across multiple industries. Therefore, smart ways to leverage co-production, storage, or arbitrage of hydrogen within wider systems could have a considerable effect on the levelised cost of e-fuel production.

Conclusions

It is yet to be determined whether electrofuels make sense in the context of our future energy system, due to their comparatively low CO2 abatement potential per unit of renewable electricity. Usage of renewable power should be directed to displacing fossil fuel generation before powering processes where the majority of electricity is wasted.

Improved research on contrails and other areas will soon enable us to paint a better picture of the climate impact of electrofuels. If this turns out to be positive, then the area may be an investment case for World Fund. However, many electrofuel startups that we see currently are not attractive for venture investment. Startups that integrate existing processes with incremental improvements and low defensibility will likely be out-competed by large energy companies.

There is also a burgeoning field of academic research in areas highly relevant to electrofuels. True innovators that can commercialise new and novel processes have the potential to capture a significant share of the SAF market. If the climate impact of electrofuels becomes proven, these investments will be extremely compelling.

.svg)

.png)